|

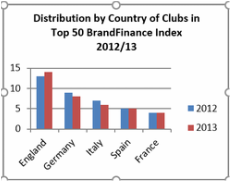

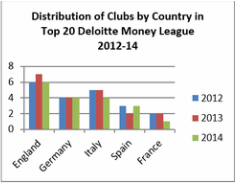

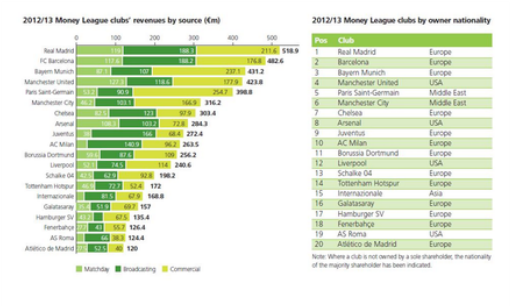

This dissertation would not have been possible without the support of the University of Hull and most importantly my dissertation supervisor Richard Andrews. Firstly the University of Hull have gave me support over the 4 years which has allowed me to progress, develop my skills and ultimately finish my degree in business management. Also I would like to further than the University for allowing me to do a topic for my dissertation which I feel really passionate about and hold a major interest in. Secondly I would to thank Richard Andrews, my dissertation supervisor, whose support and encouragement has enabled me to produce this report through his academic guidance. Furthermore the various discussions held with Richard Andrews helped narrow the ideas and thoughts down and transfer them into the final report. Abstract Financial regulation has been present in a number of European leagues for some time now and other leagues are following suit as UEFA introduce their Financial Fair Play to introduce fairness between clubs while at the same time keeping the competiveness with each club. The increased interest of football globally means every club has an opportunity to generate further revenue as they look to gain a share in the global football market. However in order to increase revenue, each club needs a respectable strong brand which will attract more fans to invest in their product. But as clubs try to develop a strong brand, they take investment risks which do not always pay off and leaves the club with severe debt on occasions. With these inevitable risks it is more important than ever to introduce financial regulation that will safeguard each clubs future. It is further important to have these regulations as clubs in some cases spend vast amounts of money in trying to achieve success as they know the reward is huge. The report provides analyses of how financial framework and brand value interlink with each other and how by implementing or not implementing financial regulation effects the league as a brand. The study comprises all of the ‘Big 5’ leagues in Europe (England, France, Germany, Italy and Spain) and compares the amount of or lack of regulation in each of the five countries in terms of income streams and total revenue, while also taking into account average attendances in each of the leagues and varying ticket prices. The literature review comprises of various sources such as recent articles, books and journals which help build up the overall picture and contribute towards a balance view which ultimately contributes to the conclusion of this thesis. The various authors cited within this text have vast amounts of experience and are widely respected within this this area which helps with the validity of the research. The methodology uses a secondary approach as this was deemed the appropriate method to use which allows the most accurate results and reasonable outcomes to be reached. Within the methodology the various approaches rely upon brand finances ‘brand value’ index which takes into account various factors in order to interpret the overall outcome that is the value of the brand. The findings take into account the results from the method along with the information gathered from the various resources used. They outline that financial regulation is a vital tool within the World of football nowadays and highlights the differing financial results within the 5 countries. 1. Introduction The aim of this thesis is: ‘To investigate the impact of the model of financial regulation in football on the successful development of the league as a brand’. This outlines the bigger problem in the football industry as brand has become of increasing, if not dominant, significance in developing its commercial exploitation reflecting its globalisation. Football is generating ever increasing revenue, especially at the top end, yet many leagues and clubs are running at increasing losses. There is also disparity in revenues within the leagues and many teams overspend to try to achieve success, although ultimately many fall short and end up in debt. However as Thompson (2013) stated it shouldn’t matter if clubs have debt as they can be seen as different from other businesses. Furthermore a number of clubs in some leagues have been bought and heavily subsidised by wealthy private investors. The football authorities at national and transnational levels are increasingly concerned about the sustainability of clubs and competitions running at high levels of debt and are introducing financial regulations to limit these losses. This thesis investigates whether financial regulation can go hand in hand with the brand through examining the following four key objectives: • Examination of the impact that the relatively well established financial regulations in the French league have had on its development as a brand. • Comparison of the French League with other variously regulated major European leagues, such as the other four “big 5” (Desbordes, 2006. P.83) (England, Germany, Italy and Spain). • Investigation of relative brand value by comparing the revenue streams of indicative clubs in the French League with those of similar level teams across Europe. • Assessment of the potential effect of UEFA Financial Fair Play Regulations on a League’s brand. From this it should possible to conclude whether financial regulations can be a positive or negative influence for the football industry and for the brand of the leagues and their clubs. Over the last 10 years finance in football has become increasingly important with some clubs spending beyond their means, subsequently going out of business. Finance in football is important to each club as this helps dictate the strength of the brand, with research into brand equity being conducted since the 1980’s, due to the competiveness and link to market value (Bridgewater, 2010). Trends in brand value and presence in the Deloitte top 20 over recent years are shown in charts 1.1 and 1.2. Further information is contained in appendices 1.A & 1.B.

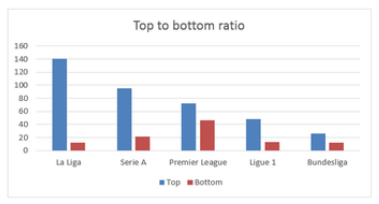

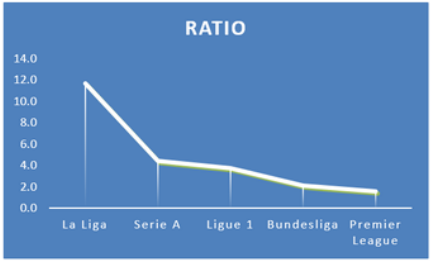

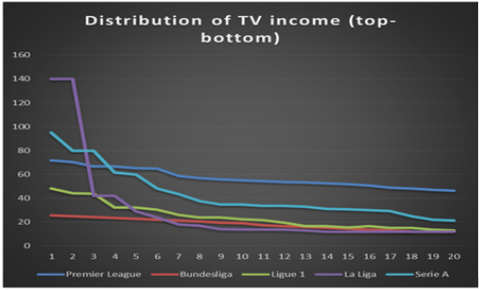

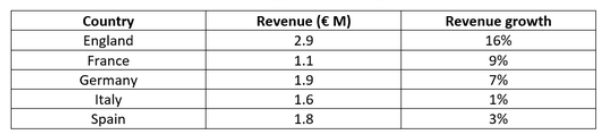

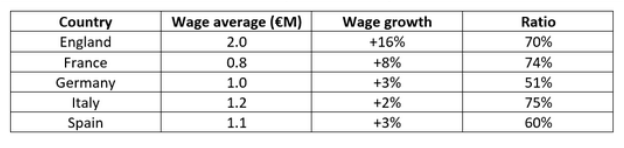

With this has come a need to monitor finance in football as according Hamil and Walters (2010) European football significantly lacks profitability and financial management, with King (2011) stating that financial troubles have followed as a despite income rising in the ‘Top 5’ leagues. Many argue that financial regulation is unnecessary and clubs should be allowed to control their own affairs, with owners, fans and shareholders backing their club regardless of the financial state it is in. However recent work by Beech (2008) states that despite an increase in revenues many clubs still operate in the red and that the situation in England mirrors that of European football in general with Italy being one of the countries with the worst financial management, the other, according to Gomez et al (2011), being Spain. Andreef (2007) reports that despite rising debt levels within the Spanish game, clubs increase spending on transfer fees and player wages. This view is echoed by Kuper and Szymanski (2012) who state that many supporters have been worried about their clubs financial state for over a decade, with people becoming increasingly worried after the recession. An example pointed out by Kuper and Szymanski is that Chelsea and Manchester United’s combined net debt levels when they met in the 2008 UEFA Champions League final stood at £1.3 billion. This was a worrying sign, so worrying that in 2009 UEFA President Michel Platini stated that if this trend continued it would not be long before major European clubs faced going out of business. These concerns have been taken seriously as in 2012 UEFA announced their intention to introduce Financial Fair Play (FFP) which would mean clubs would have to be more stringent with their finances. However, contrary to Platini’s concerns, Kuper and Szymanski (2012) state that the idea of football clubs being “inherently unstable” (Kuper & Szymanski, 2012. P.81) is wrong as they rarely go bust despite being “incompetently run” (Kuper & Szymanski, 2012. P.81). Furthermore Kuper and Szymanski (2012) state that the various football authorities worry too much about finances of clubs and are often concerned about the wrong clubs. This sentiment is supported by a comparison between the 1923 English Football League and the 2007-2008 season, where 97% of clubs (85 clubs) that competed in 1923 still competed today. Furthermore 75 of the clubs still remained in the Football League (top 4 divisions) and quite astonishingly 48 of the clubs were in the exact same division as 1923 (please note this may of changed from 2008). Also only 9 clubs from 1923 had moved divisions by 2 or more. These figures support Kuper’s and Szymanski’s argument that football clubs are unstable but rarely go bust, which begs the question should financial regulation be for all clubs in the beautiful game or not? Furthermore if European clubs’ debt did cause them to collapse then “surely there would now be virtually no European football clubs left” (Kuper & Szymanski, 2012. P.89). However Beech, Horsman and Magraw (2007) argue that recent research has shown worrying incidence of English clubs facing insolvency. Between the years of 1986-2007 there have been 56 clubs becoming insolvent (68 in total as it happened more than once with some) (Beech et al, 2007). In part the figures were influenced by ITV Digital’s (then TV rights broadcaster) collapse in 2002 which had a disastrous effect on the Football League clubs, however Hamil and Chadwick (2010) state that more significant factors affecting solvency were poor on field performance and relegation. The main problem Hamil and Chadwick (2010) identify is that English football has failed to deal with the commercialisation of the sport, since only in the last 10 years have clubs “come to terms with a post-commercialised phase” (Hamil & Chadwick, 2010. P.260). However whilst the Premier League has adapted to the business needs of the industry, this has been not entirely successful. Despite the considerable revenue streams which have been created and spent by clubs, the control of costs to guarantee profit has proved very difficult. Financial sustainability has consequently appeared on the agenda of regulatory bodies. Most notably UEFA has introduced Financial Fair Play (FFP) criteria for the 2013-14 season, which restricts clubs to a €45M cumulative loss over 3 years and a maximum loss (if the owner does not inject equity) of €5M over the same period (Thompson, 2013). Participation in UEFA’s club competitions (Champions League & Europa League) (UEFA, 2014) is dependent on meeting these requirements with UEFA monitoring each clubs accounts for compliance. Furthermore, according to Conway (2014,) clubs cannot spend more than their generated revenue and they are expected to meet all their transfer and employee payment needs. The sanctions in place for any club breaching the rules range from warnings and fines to a ban from UEFA competitions. An investigation of 76 clubs competing in this season’s (2013/14) Champions League and Europa League thought to be breaching the regulations has been completed although the evidence will not be released until the end of the season with the first action being taken in April 2014. Michael Desbordes has researched financial regulations in the French league over recent years. Desbordes (2006) states that the French method of managing finance is unique and aims to avoid bankruptcies part way through the season, which makes the league a “true championship” (Desbordes, 2006. P.86). Similar systems to the one in French football are used in rugby, handball and basketball. The Direction Nationale du Contrôle de Gestion (DNCG) is the system which monitors French football finance and is an internal commission to the French Football Federation (FFF). Desbordes (2006) cites that the system acts like “French football’s policeman” (Desbordes, 2006. P.86). The tight financial regulations tie into increased value of TV deals with Desbordes (2010) stating that Ligue 1’s TV deals have increased from the end of the 1990’s through “two successful deals” (Hamil & Chadwick, 2010. P.303). According to Repition (2008) the deal signed in 2008 enabled clubs to share €668 million. Furthermore the latest deal signed in April 2014 for the 2016-2020 seasons saw the sum increase again with the rights for Ligue 1 going for €726 million and the Ligue 2 (2nd tier) for €22 million each year (LFP, 2014). Comparison with the Spanish League (La Liga) shows a contrasting situation with looser financial regulations and many clubs in the top flight holding severe debt. However according to Ascari and Gagnepain (2006) Spanish football has seen significant economic activity with its matches being well attended. This is supported by statistics which shows La Liga had the 4th highest average attendances for the 2007/08 season in Europe (Deloitte, 2009. P. 14), and the 3rd largest revenues overall from TV broadcasting (Deloitte, 2009. P. 13). However there is a lack of competitiveness since up to the 2007/08 season, 77 league championships had taken place, but only 9 teams in that time won it. Indeed 3 of the 9 have only won it once (Sevilla FC, Deportivo de la Coruna & Betis) with the majority of league championships going to either Barcelona or Real Madrid (Hamil & Chadwick, 2010). Marti et al (2010) state that the increasing wealth generated by a few football clubs in Spain could lead to an increasing imbalance in the league. Marti et al (2010) suggest further that participation in International competition goes someway to explaining the financial imbalance with only a few clubs obtaining a large amount of money. Gomez et al (2008) supports this view by acknowledging that the “existence of an elite International competition (e.g. UEFA Champions League), automatically creates imbalance in the national competitions” (e.g. La Liga) (Hamil & Chadwick, 2010. P.267). Italy is another of the ‘big 5’ leagues with financial difficulties. This is evident in the recent Deloitte Money League (2014) which states that Italian clubs, apart from Juventus, are struggling to grow resulting in them sliding down the Money League. Deloitte (2014) highlights the fact that with the majority of clubs not owning their stadiums this makes it difficult for them to generate match day and commercial revenue on par with other clubs in the ‘big 5’. Furthermore Cherubi and Santini (2010) echo this view by stating that the economic financial situation is dire in every area apart from broadcasting income upon which clubs are “highly dependent” (Hamil & Chadwick, 2010. P.291). However it is worth noting that like Spain the country’s poor economic climate has had an impact. Germany on the other hand has tighter regulations like France with many clubs being debt free. This is partly down to the various governing bodies which regulate different levels of German football. These governing bodies include the German Football Association (DFB) which regulates the game generally, then within that is the Fussball Liga GmbH (DFL) which governs the Bundesliga (1st & 2nd tier). According to DFL (2008) the annual turnover of the Bundesliga in 2007 was €1.45 billion, with Buhler (2010) stating that the Bundesliga is “considered one of the most business-like leagues in the World” (Hamil & Chadwick, 2010. P. 327). Buhler (2010) states that German football saw major growth throughout the 1980’s with the introduction of privately owned TV companies, which led to more competition in the broadcasting market resulting in higher income streams for the clubs. A further rise in revenue from broadcasting rights was seen in the 1990’s with the introduction of pay-per-view. Other success factors in Germany include high attendances and cheap ticket prices which in turn help generate healthy revenue. Financial regulations are also being introduced in England with FFP applied to the English Premier League and Championship (1st & 2nd tier) for the 2013/14 season. This supplements existing regulations for England’s League 1 and League 2 (3rd & 4th tier). The Premier League FFP include a maximum of permitted losses of £105M over 3 seasons, while the maximum loss is £15M should the owner not inject equity (Thompson, 2013). There are no restrictions on wages if they are below £52M per annum. Each club will be monitored through their annual accounts along with the clubs’ projections which will be submitted to the Premier League at the end of each season. An aspect of financial regulation is the effect on the brand. Bridgewater (2010) looked into the development of football as a brand. The importance of brands to business and to marketers has increased over recent decades with developments in branding in a broader range of sectors (public sector, charities & e-markets), which ultimately gives the customer something that they can identify with. Brand value in football has an essentially emotional basis. Bridgewater (2010) examined the evolution of the support base from local allegiances in early times into modern global tribes, i.e. groups with shared interests. Part of the value to the supporter was suggested as lying in the escapism and the sense of belonging to a community that it offers. Furthermore Cova (1997) identified the role of the shared interest amongst the supporters and the effect on their self-esteem and suggested that brand value lies in a product’s “linking value”, that is its ability to bind this wider community. One example of this is Manchester United whose global marketing strategy has made it as familiar globally as Coca-Cola. Bridgewater (2010) states that the “sporting world has long recognized the fervent loyalty of fans” (Bridgewater, 2010. P.2) concerning a certain team or a sporting icon. This view is illustrated by League Two (4th tier) Luton Town taking 40,000 fans to Wembley for their Johnstone’s Paint Trophy Final. However commercial significance also plays a key part in brand growth. The view of brand being vitally important in the sports industry (particularly football) nowadays is outlined by Ozanian (2005) who stated that the global sports market is worth around $12 billion per year, whereas Bridgewater (2010) stated that the sports market in the United Kingdom in 2008 was estimated to be worth £21.2 billion and growing year upon year. Furthermore Haigh (2013) states the average amount of money paid by sponsors to be associated with 1 of the top 50 clubs increased in 2013. The analyses for this thesis will be based on secondary data relating to the two complementary strands of finance and brand value. By drawing on published data this approach should ensure more accurate, and in some cases tested, information on which to make comparisons. Furthermore the use of secondary data is less time consuming compared with that of primary as there is no use of interviews, which also means there is no reliance on an extra party which may have a detrimental effect on the research, for example through bias or context. Although the thesis uses secondary data only, the researcher has not neglected the HUBS ethical procedures and abided by all the rules (see appendices A for ethics proforma.) In assessing the ‘Big 5’ leagues the factors to be considered are the regulatory framework including the negotiation mechanisms for broadcasting rights; financial indicators such as the value, sources and distribution of revenue, and profitability; and indicators of brand value of the leagues and the clubs such as attendances, commercial and broadcast revenue and sporting competiveness of the leagues. The information is taken from published sources such as core texts and articles relating to football finance and the annual reports of the governing bodies such as UEFA, which should be considered to be reliable and authoritative. Another resource is the index analyses by BrandFinance which assesses the strength of clubs as a brand. The index analysis helps to “benchmark strengths, risks and future potential compared to their competitors” (Haigh, 2013. P.27). Clubs are rated from AAA+ to D for brand strength (strong to weak). Key Performance Indicators (KPI’s) are also used in this to distinguish whether or not a club has a strong brand. These KPI’s consider 5 factors, namely the star players at the club which drive sales of the merchandise; the stadia in which the club’s “product is showcased” (Haigh, 2013. P.27); the club’s heritage which determines how loyal the fans are; trophies won, as Haigh (2013) states that “only history remembers winners” (Haigh, 2013. P.27); and the manager of the team as the club cannot have a strong brand with an un-successful manager or if there is managerial instability within the club. Deloitte’s Money League provides a method for comparing a club’s financial strength. Deloitte releases the Money League annually enabling comparison against previous years to test a clubs success both on and off the field. There are various ways in which relative wealth of clubs can be determined although these can be limited by information not being in the public domain. Deloitte (2014) has developed models which help to predict clubs future cash flow which assists sellers and potential investors. The easiest way according to Deloitte (2014) to test a clubs wealth is through revenue which is the easiest comparable information as well as it being widely available. The following sections outline the various regulatory bodies in each of the ‘Big 5’ countries, indicators of financial health and measures of brand value from various teams across the ‘Big 5’. Ticket prices and attendance figures are also considered. Appendix 4.A shows the Deloitte (2014) Money League analysis of top 20 teams accompanied by a table it showing the country that the majority shareholder is from. The value of TV revenue within each league and its distribution is included as a measure of financial performance and is shown in figures 4.1, 4.2 and 4.3 below, which enables comparison across the leagues.  Figure 4.1 TV revenue distribution €M (top-bottom).  Figure 4.2 TV revenue distribution ratio (top-bottom)  Figure 4.3 Distribution of TV income €M (top-bottom) 4.2.1. Regulatory Framework In France the clubs’ finances are monitored by the DNCG. This organisation requires the member clubs (top 5 divisions) in the league pyramid to submit their accounts at the end of the season. If a club fails to abide by the rules the sanctions that the DNCG can impose include point deductions and demotion of leagues and in some cases expulsion. France’s TV rights are distributed evenly thus mirroring that of England and Germany. The rights are split 50:25:25 with 50% being split in equal parts, 25% based on the television audience and 25% on sport merit which is related to the clubs previous seasons positions. 4.2.2. Financial Performance Many clubs in France still have debt with an increase from 2011-12 season. The average club debt overall was €60M, however 3 of the 20 clubs in Ligue 1 did have positive results. Ligue 1 revenue rose €1.27 Billion (11.4%), but this was predominantly down to PSG and their relationship with Qatar Tourism Authority.

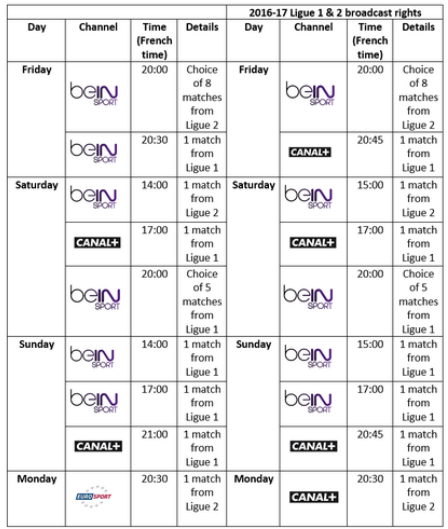

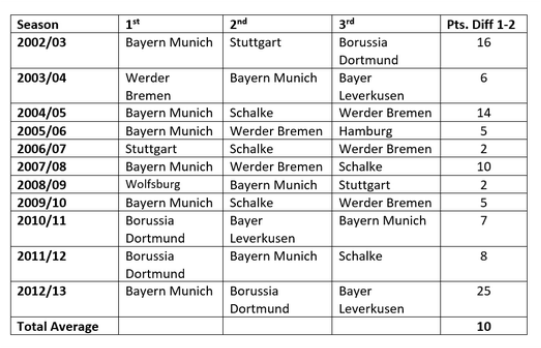

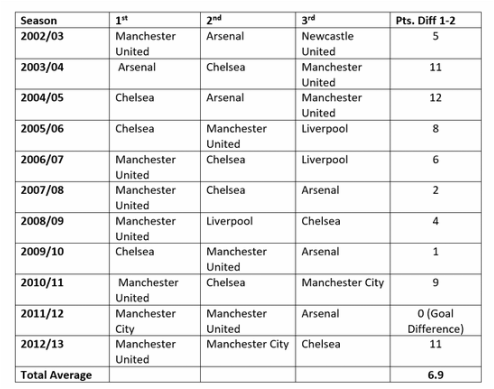

4.2.3. Brand Value The French league has fared the worst out of the “Big 5” as some teams cut back finances due to lack of on the field success. There are only 4 out of 20 Ligue1 clubs in the top 50 and a worrying sign is all the 4 brands have decreased in value. The Deloitte Money League 2014 (Deloitte (2014)) shows only one French team in the top 20 (PSG) with Marseille dropping from 17th position down to 30th, while Lyon have even fallen outside the top 30 due to missing out on a Champions League place. In comparison the previous Deloitte Money League (2013), placed 2 French Clubs in the top 20 (Olympique Marseille and Olympique Lyon), whereas in 2014 only PSG features. Based on the 2013 Money League, Marseille’s revenue dropped by 10% to £109.8M with the club having a mixed season on the pitch. Whereas Lyon for 2011/12 saw revenue drop by 1% to £106.7M due to decreases in both match day and commercial revenue with them having the second lowest matchday revenue in the Deloitte Money League top 20 2011/12. However this decrease was offset by Lyon’s rise in broadcast revenue. Their main failing was finishing 4th in their domestic league meaning failure to qualify for the Champions League for the first time since 1999. The prediction in Deloitte’s Money League (2013) that Lyon would struggle to maintain a top 20 place for the Money League in 2014 has been proven right. PSG’s revenue has grown substantially from £178.4M in 2012 to £341.8M in 2013. Contributing to this was the acquisition of global brand name David Beckham. Paris Saint-Germain is the highest ever French team in 5th place of the Deloitte Money League due to their “record turnover of €400 Million” (Deloitte, 2014. PP. 18) due to the enhancement of their global brand since the Qatar Sports Investment takeover in June 2011. Kay (2014) states that UEFA’s FFP will test them, having only being allowed to make loses of £37 million. However according to Kay (2014) they have signed a deal with Qatar Tourism Authority worth £570 million over 4 years which should cover their accounts for the years 2012 to 2016. The challenge however is whether UEFA deem the sponsorship unfair due to a possible connection with the owners. In comparison another French giant, Marseille, has been towards the bottom of the Deloitte Money League for the previous five years having peaked at 14 and as low as 16. Despite Marseille winning the League Cup and managing to reach the ¼ finals of the Champions League, the club finished a disappointing 10th place meaning that they only qualified for the UEFA Europa League as virtue of winning the cup. Furthermore the renovations at Marseille’s stadium caused the capacity to be reduced temporarily resulting in a drop in match day revenue by 29% to £14.6M. Ticket pricing influences the picture. Spiro (2013) states that inflated prices are not an issue in France as the clubs try to attract as many fans as possible since only a minority of games sell out. Furthermore Spiro (2013) outlines that for the majority of Ligue 1 teams, spectators can get in for less than €20 (£16.70), with a number of teams allowing spectators in for half of that. It is also worth noting that due to their recent success Paris Saint-Germain has seen an increase in season ticket holders from 10,000 to 31,000. This is despite prices rising at the Paris based club with prices rising over the last 2 years by 11% and 30% respectively. A future impact on the French Ligue 1 brand is the importance of broadcasting rights. The new deal starting from 2016 will provide even more money to share between the teams. This sees a 20% rise from the previous contract, with LFP president Frederic Thiriez stating he wants a “league on the podium of the three best European nations” (LFP, 2014) behind Germany and Spain. Thiriez further states that the deal sees the LFP keep their two major broadcasting partners (Canal+ & BeIn Sports) for the next six seasons. Furthermore by having a record sum for the seasons of 2016 to 2020 its makes “Ligue 1 one of the most valuable leagues in the Word” (LFP, 2014), which can only be seen to enhance the brand. More detail on the new deal can be found in Appendices 4.B. 4.3.1. Regulatory Framework Germany has a similar system to France in that it monitors clubs finances through their submission of accounts and transfer documents. Punishments in Germany should a team enter the red involve point deductions and transfer embargos. The system was created by the DFL and acts as a prototype for UEFA’s licensing scheme as well as being seen as a beneficial model to other countries. The criteria monitored by the DFL include five categories (sporting, infrastructure, personnel and administration, legal and financial) (Buhler, 2005). In 2007/08 as a result of these strict regulations all 18 Bundesliga clubs were financially stable and reporting profits (DFL, 2008. P.173), thus highlighting its success. Broadcasting rights are negotiated between the DFL and broadcasters which allows the revenue to be distributed evenly amongst the clubs in the Bundesliga. 4.3.2. Financial Performance Germany had the second biggest revenue growth out of the ‘Big 5’, these results can be seen in appendices 4.E (4.F shows wage average). The Bundesliga’s main growth in revenue was the success of commercial deals which accounted for over half of the clubs revenue.

4.3.3. Brand Value Germany has seen growth with 8 out of the 18 Bundesliga clubs in the top 50 brand with one of the clubs holding top spot. The strength of the Bundesliga looks set to continue growing with Bayern Munich’s rise and the emergence of Borussia Dortmund. Germany is emerging as one of the most successful leagues in the World, with its recent success coming to fruition after the country hosted the 2006 World Cup. In 2006/07 the clubs in the Bundesliga derived 21% of revenue on average from matchdays, which amounted to €17.2 million (Hamil & Chadwick, 2010. P.330) and recorded the highest attendances throughout Europe with an average of 37,644 fans attending each game. There has been further growth over recent seasons with the 2012/13 season attracting on average 41,941 people per game (12.8 million over the entire season) (Lovell, 2013). Ticket prices are considerably lower than the other ‘Big 5’ leagues and encourages season ticket uptake. This is supported by a BBC survey in 2013, with Lovell (2013) stating that for the 2013/14 season the cheapest match day ticket was at Bayer Leverkusen which cost €10 compared to the most expensive ticket which is found at Hertha Berlin for €89. Low ticket pricing contributed to teams such as Bayern Munich, Borussia Dortmund and Schalke playing in front of sold-out stadiums each week, potentially maximising revenue. Whilst Bayern have been able to generate high grossing commercial revenue for many years (Deloitte (2014), they have recently been overtaken by French club Paris Saint-Germain. Despite this Bayern’s commercial revenue accounts for 55% of total revenue and increased by €35.5 million during the last financial year (Deloitte, 2014). Bayern also saw an increase in broadcast revenue by €25.6 million, thus overtaking Manchester United in the Deloitte (2014) Money League. The Deloitte (2014) Money League and the Haigh (2013) BrandFinance annual report confirm that Bayern Munich are a dominant force within football through impressive revenue streams enabling the club grow as a brand. As Haigh (2013) states Bayern’s “tremendous domestic and European season” (Haigh, 2013. P.3) has helped them achieve number one brand status in the World of football and a brand rating of AAA, overtaking Manchester United. Internal comparison with Bayern’s German rivals shows an overwhelming strength in terms of revenue and brand. According to Haigh (2013) Borussia Dortmund is the second strongest brand overtaking Schalke after many years of hardship and financial turmoil. The change in brand value saw Dortmund’s rise by 15% ($227M in 2012 to $260M in 2013), whereas Schalke’s decreased by 3% ($266M in 2012 to $259M in 2013) (Haigh, 2013. P.4). A factor in Dortmund’s development as a brand is their rise in attendance over the period 2008/09 to 2012/13 from 74,626 to 80,503, reported by Bond (2013). As with Bayern Munich, commercial agreements are key in increasing the club’s brand with Dortmund recently agreeing a long-term marketing agreement with Sportfive as well as extending the stadium naming rights deal with German financial service Signal Iduna. On the field success from domestic success in 2011/12, combined with managerial stability has also helped to develop a strong brand. However Haigh (2013) states with the success Jurgen Klopp is having at Dortmund it may not be too long before other clubs try to poach Klopp, which could have a detrimental effect on Dortmund’s brand. 4.4.1. Regulatory Framework Recently to coincide with UEFA’s FFP, and financial regulations in the leagues below, the Premier League has introduced financial regulations which over a number of seasons aim to improve the clubs debt levels and increase competition. The new rules require clubs to break-even with only a certain amount of the owners investment allowed to count as equity. The Premier League (2013) states that these regulations are “designed to further improve sustainability of clubs” (Premier League, 2013). TV rights are negotiated collectively with revenue spread between the clubs 50:25:25, with 50% being distributed evenly, 25% based on the clubs final league position and the other 25% for the amount of television games a club has (Premier League, 2013). Overseas rights are shared evenly. 4.4.2. Financial Performance The Premier League according to Deloitte (2013, B) is the football world’s leading generator with clubs revenue growing by 4% in £ (16% in €). · Only 8/20 clubs made a profit · Annual revenue: €2500m · Revenue per game: €6.579m · TV income: €1,147m · Range and ratio of TV income share: 71.8 to 46.3 €million / 1.6 4.4.3. Brand Value England’s Premier League arguably has the best brand in the world as it attracts massive global interest, as evidenced by the pre-season tours to Asia by a dozen Premier League clubs each year. The Premier League has the most expensive ticket prices when compared to the other four countries from the ‘Big 5’ leagues. Season tickets can cost up to £1,000 with match day tickets costing £30 on average. The amount of money the Premier League receives for TV rights is substantial. The latest deal saw the Premier League receive £3bn (Hartnett, 2013), which according to Deloitte (2014) will see the English teams rise up the money league in the future, thus improving the clubs and the league as a brand. For example it is estimated that Manchester United’s various commercial activities along with the new broadcast contract will see the club’s revenue to increase above £400M for the 2015 edition of the Money League (Deloitte, 2014). Deloitte (2014) also states that for the 2015 edition it expects to see all Premier League clubs report healthy revenue, with the likes of Liverpool and Tottenham (12th & 14th respectively in the money league) likely to move up. Furthermore Premier League teams currently outside the top 20 are likely to move up and add to the current record of eight clubs from England. The Premier League has the most clubs within the top 50 brands further emphasising its global appeal. However with UEFA FFP coming into effect at the end of the season it is estimated this will adversely affect the Premier League. Arguably the biggest brand in the Premier League is Manchester United, but with other clubs spending power gazumping that of United, could they lose their grip as England’s most valued brand? It is also not helped by managerial change after stability for over two decades at the club. Richard Scudamore (Premier League C.E.O), expressed concern that Manchester United’s recent poor on the field form is having a detrimental effect on the Premier League’s global brand (Bascombe, 2014). One club which may eventually overtake Manchester United, is Manchester City who themselves saw a 10% increase in their brand value this year while United’s decreased by 2%. However UEFA FFP will impact upon City’s future spending as a recent Sporting Intelligence survey (Harris, 2014) shows that their average wages increased by $6 million within the last 4 years, which is a trend that cannot continue. Another trend that cannot continue is the managerial instability with a manager being replaced on average ever 2 seasons as they are expected to win at least 1 trophy per season. As Haigh (2013) states Manchester City need to find alternative revenue streams to make the club sustainable as UEFA FFP prohibits clubs from spending more money than they earn. However Manchester City has signed a number of lucrative commercial deals, including the £12 million per season deal with kit supplier Nike. Further proof that the blue half of Manchester is developing as a brand can be seen with their pre-season tours to Asia each season as well as recently founding a Major League Soccer Franchise, both of which will only enhance their appeal Worldwide. 4.5.1. Regulatory Framework Football in Spain has suffered from debt for some time due to the lack of regulation. However at the start of the 2013-14 regulations were introduced by the Spanish Football Federation and the National Sports Council which requires each club every season to provide information on budget expenditure and revenues, budget funding, investment and divestment as well as a projected income statement according to Football Espana (2013). If a club fails to meet this criteria then they will be unable to sign a player and budgets will also be capped based on income levels. The reason for the introduction is to “contribute to the economic and financial sustainability of professional football, preventing situations of economic instability” (Football Espana, 2013). Broadcast rights have caused huge disparity between clubs at the top and the bottom as the rights were negotiated on an individual basis rather than collectively meaning bigger clubs (Barcelona & Real Madrid) could get the biggest slice. However in the future the league will negotiate rights on a collective basis and shared accordingly. This law was pushed through by the Spanish government which will see an increase in competition between clubs and improve their finances (ESPN, 2013). With the old system Barcelona & Real earned €140 million each compared with Real Vallecano who received €14 million. The third highest earnest was Atletico Madrid who made €47 million (ESPN, 2013). 4.5.2. Financial Performance Barcelona and Real Madrid generate double the revenue of any other La Liga team, thus causing in balance in competition. · Total revenue: €1,622m · Revenue per game: €4.268m · TV Income: €560m · Range and ratio of TV income share: 140 to 12 €million / 11.7 4.5.3. Brand Value West (2013) states that match day tickets in Spain are on average cheaper than in the UK, however this is partly down to the economic problems within the country. However tickets are still unaffordable to some according to West (2013). Comparing the top 3 sides in Spain (Atletico Madrid, Barcelona & Real Madrid), Barcelona have the lowest ticket price at €15 while Real Madrid have the most expensive out of the 3 teams at €28 (Lovell, 2013). Despite, the relatively cheap ticket prices the country’s current economic conditions continue to hamper the growth of the Spanish clubs as a brand with Barcelona’s decreasing in value according to Haigh (2013) by $8 million to $572 million. However Real Madrid’s brand value has increased to $621 million, which is a rise of 4% on the previous year (Haigh, 2013) as a result of high commercial revenue, with the club selling 1.5 million shirts alone. Additionally the international tours that Real Madrid participate in further enhance their brand and increase their share of the global market. However the brand has suffered managerial instability due to the manager (Jose Mourinho) departing the club. The Madrid brand will also be hampered in future years with the announcement that media rights will be negotiated on a collective basis, rather than being negotiated individually since Madrid is one of the clubs that gets to pick the best deals. Despite this Madrid still harvests the biggest revenues in the world of football, $513 million to be precise. In contrast Barcelona, who despite only suffering the slightest decrease in brand value this year (1%), secured domestic success in 2012/13. One way Barcelona are looking to increase their brand is through the acquisition of Brazilian starlet Neymar as they believe he is “hugely marketable” (Haigh, 2013. P.10). Haigh states that the strengths of Barcelona will only help them in the long-term having agreed deals with Coca-Cola and Audi, as well as illustrating strengths in cutting costs. This will also help them meet UEFA’s FFP. Furthermore Barcelona saw a revenue growth to €494 million, however Haigh (2013) states that there is still a gulf between them and Real Madrid with Barcelona never having been the most valuable brand. A further example is Valencia which is the 3rd best brand having seen their value increase by 22% from $68 million in 2012 to $83 million in 2013 (Haigh, 2013). However despite this growth Valencia have dropped down the ranking to 26th, thus emphasising the gulf between Barcelona and Real Madrid and the other teams in Spain. 4.6.1. Regulatory Framework The Italian league seems to lack any real framework which is evident with the number of struggles and scandals affecting clubs in recent years. TV rights are assigned in accordance to various criteria with an advantage to the middle /small sized clubs, but also keeping the bigger clubs happy, thus keeping the status quo. According to clubs TV rights up until 2000 were managed collectively, however pressure from bigger clubs meant it’s now done on an individual basis. Although this is only for private television as the league does still negotiate with public television. 4.6.2. Financial Performance Italy is heavily dependent on TV income and generates the lowest match day revenue out of the ‘Big 5’ · Total revenue: €1532m · Revenue per game: €4.032m · TV Income: €892m · Range and ratio of TV income share: 95.1 to 21.4 €million / 4.4 4.6.3. Brand Value In Italy a club’s brand can be significantly affected by a poor league campaign as shown by Italian club Internazionale Milano (Inter) with a decreased brand of $151 million in 2013. By comparison in 2012 Inter’s brand was valued much higher at $215M, meaning a change of -30%. AC Milan meanwhile experienced similar problems with a dip in form over recent seasons and falling attendances which in turn brought AC’s brand value down in 2013 to $263M compared with $292M the previous year. Furthermore the stadium (San Siro) which is the home to both teams is ageing and losing the appeal which drew in big crowds in the 1990’s, which may further affect the brand negatively in future seasons. However AC’s brand rating is AAA-, which is slightly better than Inter at AA+. The analysis suggests that AC’s better brand rating is down to heritage being founded before Intern as well as winning more trophies than their rivals. However Haigh (2013) states that AC may decrease further in value due to not owning the stadium. However Inter are planning on building their own stadium and follow Juventus’ model, which looks set to become Italy’s strongest brand in the next few years. One of the reasons for Juventus strengthening brand is through owning their own stadium, which is a first in Italy. This allows the club to develop more revenue streams, especially match day. Also Juventus in the top 50 has the 5th highest brand rating with AAA-, but are 13th with their brand value of $180M, which is an increase of 20% from 2012. From Deloitte (2014) it is clear that Juventus appears set to cement itself as Italy’s top club having had consecutive successful seasons over the last few years. Deloitte (2014) shows a rise by Juventus into 9th moving above both Milan clubs in the process to become Italy’s leading revenue generating club. By comparison to Deloitte (2013) Juventus were 13th and 3rd out of the Italian clubs, in the Money League, generating £158.1M in revenue. Deloitte (2014) outline that Juventus’ main success driver was their UEFA Champions League Campaign as well as a broadcast revenue growth to €166M (up by 77%), which was mainly a result of UEFA’s distribution of tournament money. Surprisingly despite only advancing to the ¼ of the Champions League (12/13), Juventus received the highest distribution from UEFA of all the participating teams receiving €65.3M. Furthermore Juventus will see further benefit from Italy’s drop in the UEFA coefficient rankings meaning only 3 rather than 4 teams being able to qualify for the Champions League. This gives Juventus an even “bigger share of the Italian market pool” (Deloitte, 2014. P.23) as a result. Furthermore Deloitte (2014) support Haigh’s (2013) view that Juventus have benefited from owning their own stadium having seen match day revenue at the new stadium treble since opening in 2011. Additionally Juventus are expected to increase their revenue due to the new commercial agreements signed with the FIAT Jeep brand and a new kit deal with Adidas (replacing Nike) which will last for six years. Further deals with the Italian club include Samsung and Bwin with Deloitte (2014) predicting that these will help Juventus cement a top 10 position in future Money Leagues. However a negative within Italian football is financial regulation (or lack of) which affects the majority of Serie A clubs. Also attendances are declining in the Italian league having decreased by 1 million compared to the previous year according to a report prepared by the Italian Football Federation. Italy’s league attendances only exceeded France’s Ligue 1 after attracting 22,591 compared to France’s 19,211 per game. Furthermore the clubs’ revenue from the stadiums decreased by 4.1% (Armagio football stats, 2014). Italian football clubs are highly dependent on the broadcasters (Cherubini & Santini, 2010) which provide the majority of their income. Deloitte (2002) conducted a survey which showed that football is Italy’s most popular sport with a TV audience of over 22 million. This dependency on the media and broadcasters is highlighted with AC Milan's loose relationship with Mediaset and Torino’s with Cairo Communication. Supporting data provided by Lega Calcio emphasises the relationships between the media and football in Italy and shows various phases across the decades in the disparity between the top two leagues regarding revenue distribution. For example the 5 phases ranging from the early 1980’s show that the revenue distribution system was equal until phase 3 in 1996, where Serie A & B shared equal proportions. The Brand Finance (2013) report places Bayern Munich as the top brand at $860M overtaking Manchester United, which drops to second at $837M with the club mainly effected by managerial change albeit retaining their the AAA+ rating. Another German team, Borussia Dortmund, has increased its brand value by 15% to $260M compared to 2012 (Haigh, 2013). Brand Finance (2013) also notes that the Italian and Spanish brands have been affected by the recent economic conditions and that in France all the 4 teams in the top 50 have a decreased brand position with Marseille being the highest placed team in 18th with an AA- rating with a change of -34% (Haigh, 2013). Overall however brand value has seen a 7% increase across the top 50 clubs, thus showing that football is “recession proof” (Haigh, 2013. P.3). Within the top 50 brands the English Premier League has 14 teams which underlines the strength of the league as brand. Another loosely regulated league, Spain, only has 5 teams in the top 50 brands with a big gulf between Real Madrid and Barcelona and the other teams in La Liga. Italy is another country that is unregulated and like Spain has been suppressed by the economic conditions recently, although they have fared better than Spain with 7 clubs in the top 50. Analysis of the closeness of the title races across the leagues suggests that there is little relationship between regulation and the winning points gap, but the Bundesliga has involved more teams that the others in the top three places suggesting more open competition.(appendices 4.E-4.I). The introduction of UEFA’s FFP will requiring clubs to do either or both of increasing revenue or reducing costs. However Deloitte (2014) predicts that the “disciplined and responsible governance” (Deloitte, 2014. P.6) will help rather than hinder clubs and believe this approach should only be encouraged. However only time will tell what sort of impact these regulations will have on a club’s brand. One can suspect it will favour some clubs (most likely from the countries with regulations already in place) in their quest to rise up the money league ranking as well as improving their brand value. Comparison with the highly commercialised US market with American football (NFL) is informative. This tightly regulated franchise-based competition has collective marketing with revenue sharing and re-distribution and a salary cap to reduce disparity and enable small –medium teams to develop and compete. In 2006 Forbes estimated the average NFL team value to have increased 212% in the period 1998-2006 and average profitability increased 5-fold to $31m (Badenhausen et al, 2006). This research indicates that brand value and financial strength of the leagues is influenced by a combination of financial regulations and a quasi-regulatory approach to negotiating and distributing broadcast revenue. Whist both Germany and France have well developed financial regulations, the Bundesliga is much more successful at ensuring profitability and features far more clubs in the top 50 brands and top 20 Money League. Both have a reasonably equitable distribution of broadcast income but the Bundesliga is far more successful at attracting income from this source and in filling its stadia. Most teams are recording profit with no debt according to Bond (2013). The English Premier League has achieved overwhelming success as the leading brand and attracting broadcasting revenue in the absence of financial regulation. Contributing factors to this are the heritage of the league, the number of globally recognised clubs and the financial power to attract many of the world’s best players. A key factor in this would seem to be that as well as having the most lucrative TV contracts, the revenue is shared the most evenly across the league but in a way that rewards success whilst ensuring competitiveness. However, in spite of the success in generating revenue clubs have struggled to control costs with the result that few are profitable. The new financial regulations aim to bring this about. The less regulated Italian and Spanish leagues with less equitable sharing of broadcast revenue struggle in different respects. Decaying infrastructure and declining attendances in Italy and financial scandals have adversely affected the brand, whilst in Spain the grossly distorted TV distribution has created imbalance and lack of competitiveness although this is starting to be addressed. The Bundesliga in Germany could be considered to be the most successful league due to combining profitability with increasing revenue and Brand Value. This seems to have been an organic improvement with steady progress over many years. The tight financial regulations in Germany are a key factor and coupled with UEFA FFP the Bundesliga should continue to grow as a brand. Whist Ligue 1 in France is already strongly regulated it is not as financially stable as the Bundesliga, primarily due to its revenue base being so much lower. The recent investment into PSG has promoted wider interest in this league and is driving an improvement in brand valued PSG seems likely to continue to grow as a brand and the gap may widen between them and the likes of Marseille and Lyon. However this improvement is potentially in contravention to the French and UEFA financial regulations and so highlights a dichotomy in that without financially extending, or indeed overextending themselves, it is difficult for a club or a league to significantly improve its attractiveness. This is also reflected in the English Premier League where new owners have overspent to bring more clubs up to a competitive standard to challenge the established elite, which then adds to global and commercial interest and value. The central question is whether in the long run financial regulation will benefit the clubs and leagues by enabling them to be more sustainable financially. This leads into questioning where brand value lies. Is it with the clubs, or does the strength of the leagues by virtue of being competitive rather than dominated, add greater collective value? Regulations might be seen by the top clubs as restricting their ability to assemble the strongest sides with subsequent impact on their brand. This research shows that more clubs thrive within a more competitive league and that this is supported by a combination of reasonably even TV revenue distribution and regulation to encourage cost control. This should be important for the policy makers in the football authorities and broadcasters since two possible, alternative outcomes can be envisaged. Firstly, by ensuring a more organic system with financially sound clubs and greater competition for honours, the competitions should become as attractive as possible and enable the maximising of the collective income. Without this an increasingly small but super- dominant elite of one or two clubs in each league could emerge. These might have the best and most attractive players but be in effect playing demonstration matches against the others which might not then sustain global audiences and high broadcast revenues. In the long run this might create pressure for a trans-national elite competition to the financial detriment of the remaining clubs in the national leagues. However the risk from such a strategy that the clubs would need to consider is that it might not sufficiently interest a wider national audience as most football enthusiasts in any country would have no particular enthusiasm for the one or two elite clubs. Alternatively, whilst financial regulation would aim for sustainability and a balanced approach across the range of clubs, might this also lead to a tipping point? If enough of the elite are dissatisfied with the restrictions on their ability to attract the best players, dominate competitions and maximise individual revenue perhaps this could encourage them to break away from the current structures and set up new bodies and competitions away from these controls. Ultimately what could the authorities do? It is likely that European employment legislation for example would make it illegal for the players to be prevented from playing for non-affiliated clubs. It is considered that the brand value of a club is dependent on that of its league and vice-versa. Consequently regulations and other collective arrangements need to be sensitive to maintaining this balance with clear, effective and transparent enforcement that clubs at all levels can accept. The experience of the American NFL suggests that this should be possible and this research could be extended by further investigation of this approach for possible application to European Football. At the time of submitting this thesis UEFA has just announced that Manchester City and Paris Saint-Germain have not met the FFP criteria. However there seems to be further prevarication in the announcement of penalties which does not create a great deal of confidence for the eventual success of this initiative. Andreef, W. (2007). French Football: A Financial Crisis Rooted in Weak Governance. Journal of sports economics. P. 1-10. Armagio football stats, (2014). Football, definitely the one I'll love forever. [Online] Available at: http://armagio.tumblr.com/post/82689738198/one-million-visitors-less-than-last-season [Accessed 17 April 2014] Ascari G., & Gagnepain, P., (2006). Spanish football, Journal of Sports Economics, n.7, pp. 76-89. Badenhausen, K., Ozanian, M., and Roney, M. (2006). The Tape on the Tagliabue. Forbes. [Online] Available at: http://www.forbes.com/2006/08/31/paul-tagliabue-nfl_cz_mo_06nfl_0831nflintro.html [Accessed 29 April 2014] Bascombe, C., (2014). Manchester United's decline is bad for the Premier League, says Richard Scudamore. [Online] Available at: http://www.telegraph.co.uk/sport/football/teams/manchester-united/10728515/Manchester-Uniteds-decline-is-bad-for-the-Premier-League-says-Richard-Scudamore.html [Accessed 02 April 2014] Beech, J., Horsman, S., & Magraw, J, (2007). The Football Association’s (and the Scottish Football Association’s) changed view of financial difficulty. Proceedings of challenges facing Football in the 21st Century. Reykijavik: Play the Game. Beech, John (2008). On Tour with the Barmy Army: A case study in sports tourism In: International Cases in the Business of Sport. Oxford: Butterworth-Heinemann. Bond, D., (2013). Why Germany's new dominance of Europe may not last for long. [Online] Available at: http://www.bbc.co.uk/sport/0/football/22383346 [Accessed 07 April 2014] Bridgewater, S (2010). Football Brands. Basingstoke: Palgrave Macmillan. Buhler, A., (2010). Germany. In: Hamil and Chadwick (2010). Managing Football: An International perspective. Oxford: Elsevier. Chalabi, M., Sedghi, A. 2013. How do ticket prices for the Premier League compare with Europe? [Online] Available at: http://www.theguardian.com/news/datablog/2013/jan/17/football-ticket-prices-premier-league-europe [Accessed 04 February 2014] Champel, E., (2014). Le Pactole?, Quel Pactole? France Football, 8 April.P.37 Cherubi, S., Canigiani, M. & Santini, A. (2003) Il marketing sportive: analisi, strategi, strumenti. Milan: Franco Angeli. Conway, (2014). UEFA investigates 76 clubs over FFP. [Online] Available at: http://www.bbc.co.uk/sport/0/football/26390770 [Accessed 17 April 2014] Cova, B. (1997). Community & consumption: towards a definition of the ‘linking value’ of products or services. European Journal of Marketing, 31 (3/4), 297-316. Deloitte, (2002-2007). Annual Review of Football Finance. Manchester: Deloitte. Deloitte, (2009). Annual Review of Football Finance. Manchester: Deloitte. Deloitte, (2012). Football Money League. 1 (1), P.1-35. Deloitte. (2013). Captains of industry. Football Money League. 1 (1), P. 1-35. Deloitte (2013, B), Turn on, tune in, turnover. Annual review of football finance: Highlights. 1 (1). P.1-16. Deloitte. (2014). All to play for. Football Money League. 1 (1), P. 1-35. Desbordes, M. (2006). Marketing Football: An International Perspective. Oxford: Elsevier. Desbordes, M., (2010). France. In: Hamil and Chadwick. Managing Football: An International Perspective. Oxford: Elsevier. DFL (2008). Bundesliga Report 2008. Deutsche Fussball Liga GmbH. [Online] Available at: http://www.dfb.de/index.php?id=500016&tx_dfbnews_pil[showUid]=10685&tx_dfbnews_pil[sword]=175,926&tx-dfbnews_pi4[cat]=117 [Accessed 04 April 2014] ESPN, (2013). Spain sell collective TV rights?. [Online] Available at: http://www.espnfc.com/news/story/_/id/1486306/spain-sell-collective-tv-rights-liga-clubs?cc=5739 [Accessed 22 April 2014] Football Espana, (2013). LFP introduce own FFP regulations [Online] Available at: http://www.football-espana.net/27951/lfp-introduce-own-ffp-regulations [Accessed 16 April 2014] Gomez, S., Opazo, M., & Marti, C. (2008). Structural Characteristics of Sport Organizations: Main Trends in the Academi Discussion. Center for Sport Business Management-IESE Business School Working Paper No. 730. Gomez, S., Marti, C and Mollo, C.B, (2011). Comercialisation and transformation in Spanish top football, in: Gammelsaeter, H. and Senaux, B. (Eds), The Organisation and Governance of Football across Europe: An International perspective, Routledge, London. P.182-194. Haigh, D. (2013). Brand Finance. Fussball’s coming home: Bayern becomes football’s most valuable brand. May 2013, P. 1-35. Hamil. S. and Chadwick, S., (2010). Managing Football: An International perspective. Oxford: Elsevier Hamil, S and Walters, G (2010). Financial Performance in English Professional Football: “An Inconvenient Truth”, Soccer & Society, 11 (4): 354-372 Harris, N., (2014). Man City, Yankees, Dodgers, RM, Barca best paid in global sport. [Online] Available at: http://www.sportingintelligence.com/2014/04/15/revealed-man-city-yankees-dodgers-rm-barca-best-paid-in-global-sport-150401/ [Accessed 17 April 2014] Hartnett, J., (2013). New rights spell financial windfall for the Premier League. [Online] Available at: http://www.totalfootballmag.com/features/premier-league-features/new-tv-rights-spell-financial-windfall-for-premier-league/ [Accessed 23 April 2014] Kay, O., 2014. Financial Fair Play still does not add up. The Times Sport, 25 January. P.7. King, A., (2011). After the crunch, a new era for the beautiful game in Europe?. Soccer and Society. 11 (6), P.880-91. Kuper, S., Szymanski, S., (2012). Soccernomics. London: Harper Sport. LFP, (2014). Record sum paid for Ligue TV rights. [Online] Available at: http://www.ligue1.com/ligue1/article/record-sum-paid-for-ligue-1-tv-rights.htm Lovell, M. (2013). Price of football in Europe revealed. [Online] Available at: http://www.bbc.co.uk/sport/0/football/24086153 [Accessed 06 February 2014] Marti, C., Urrutia, I., and Barajas, A., (2010) Spain. In: Hamil and Chadwick (2010). Managing Football: An International perspective. Oxford: Elsevier. Ozanian, M. (2005). The business of soccer. Forbes, January 4th, 25-34.Premier League, (2013). Premier League, (2013). Premier League clubs agree new financial rules. [Online] Available at: http://www.premierleague.com/en-gb/news/news/2012-13/feb/premier-league-clubs-agree-to-new-financial-rules.html [Accessed 16 April 2014] Repition, I. (10th April 2008). Orange defie Canal+ dans la television payante. La Tribune. Spiro, M. (2013). Price of football in Europe revealed. [Online] Available at: <http://www.bbc.co.uk/sport/0/football/24086153> [Accessed 06 February 2014] Sportbusiness International (1st December 2008). Premiere secures Bundesliga rights. [Online] Available at: http://www.sportbusiness.com/news/168376/premiere-secures-bundesliga-rights [Accessed 08 April 2014] Thompson, E., (2013). Financial Fair Play explained. [Online] Available at: http://www.financialfairplay.co.uk/financial-fair-play-explained.php [Accessed 23 March 2014] UEFA, (2012). UEFA Club Licensing and Financial Fair Play Regulations. Nyon, Switzerland: UEFA, 2012. PDF. West, A., (2013). Price of football in Europe revealed. [Online] Available at: http://www.bbc.co.uk/sport/0/football/24086153 [Accessed 06 February 2014] Wilson, B., (2013). Premier League revenues to rise by 25%, says Deloitte. [Online] Available at:<http://www.bbc.co.uk/news/business-22766638> [Accessed 05 February 2014]

2 Comments

|