While many countries have made the decision to either cancel their current season or postpone it for at least the next couple of months, here in Poland there are already plans in place to resume the season which stopped on the 9th of March. The last Ekstraklasa (top tier) game before the lockdown was Korona’s 1-0 win over relegation rivals ŁKS Łódź. The season is now set to resume on Friday 29th May and as things stand this will be one of only a handful of European countries to have their professional leagues back up and running. The most notable re-start will be the German Bundesliga which is set to play again this Saturday (16th May), but without any fans. The Polish league (top 3 tiers to resume) and the German league (top 2 to resume) have put precautionary health and safety measures in place to ensure the players and staff working at the game are best protected. The precautionary measures for Polish football include: no spectators, a limit to 50 people in a stadium (players, staff, doctors media), two additional subs during the first 5 games for each team, two additional 5 minute breaks in the 30th and 70th minute for disinfection, and referees to have electronic whistles. So why do I believe that Polish football, specifically the Ekstraklasa, can thrive in these times? Well sport broadcasters have been forced to show repeats of past seasons over the last two months. Some broadcasters even got professional footballers from their respective leagues to play each other at FIFA in order to give the paying subscribers some of their money’s worth. Similarly, with the opportunity to broadcast live football again, broadcasters from around the world will be looking to snap up the rights for the remaining season. While the Bundesliga already has extensive broadcasting deals across the globe set in stone (€1.24bn for 2019/20 shared with Bundesliga2), this is not the case for the likes of the Ekstraklasa. Currently the Ekstraklasa receives €115m over two seasons domestically, making it the 8th most valued league in this sense. However, the Polish league has already received expressions of intent to show the remaining games of the season from broadcasters in Italy, Israel, and Portugal according to sport.pl. The league could attract further attention from higher profile broadcasters such as Sky Sports in the UK who put all their eggs in one basket with Premier League coverage. With the huge uncertainty over when and if the Premier League will resume then if Sky decided to snap up the rights for the remaining matchdays of the Ekstraklasa it would be a major coup for Poland, especially as it gives the players an increased platform to showcase their skills. That Polish football could garner increased worldwide media exposure is shown by the K-League in South Korea which resumed within the last week. Ahead of the restart of the K-League it was revealed that the league had agreed deals in 17 international markets with Australia, Germany, Austria, and Switzerland being amongst them. The K-League also broadcast one game last weekend on Twitter, which was clearly a tactic to boost interest further. This is why I think that the Ekstraklasa can gain a new fanbase in the current pandemic. While the quality might not match the likes of the Premier League, the broadcasters will be desperate to show some live sport. Also, as we have previously seen with British fans showing an interest in the Belarusian league which has continued (as apparently there you can treat the virus by visiting saunas and drinking alcohol), the fans will be less concerned about quality, they just want some live football to watch!

0 Comments

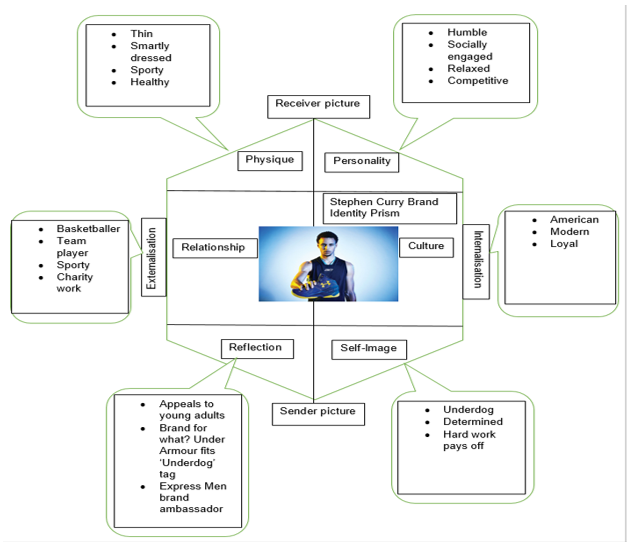

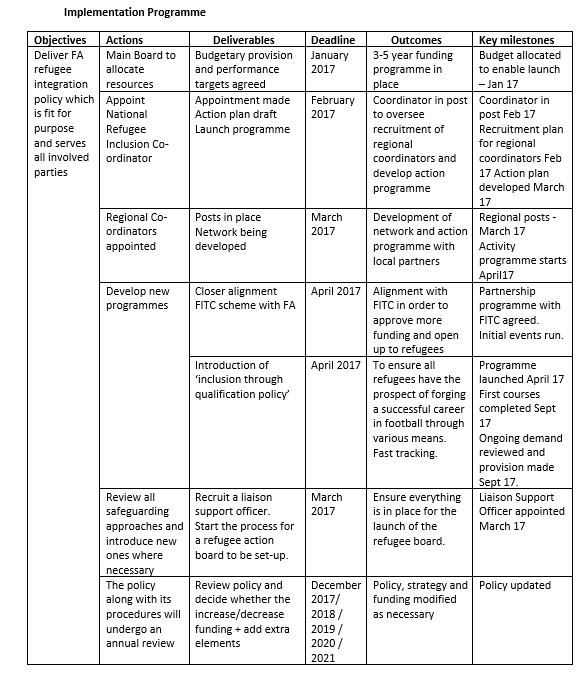

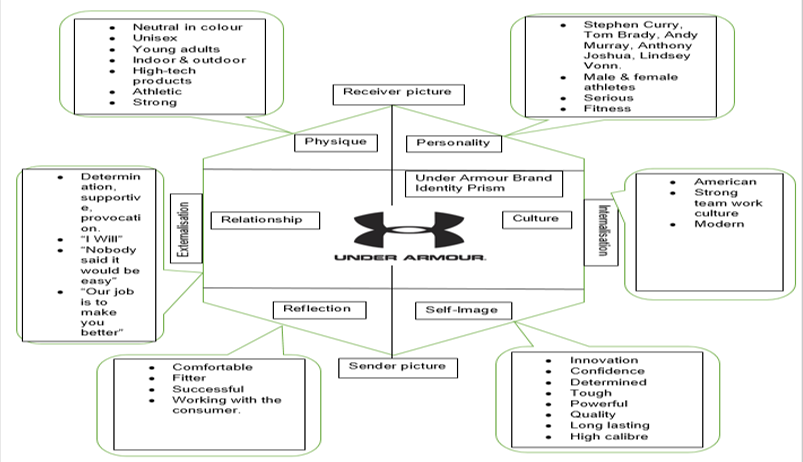

Purpose This policy supports the national programme for integration of refugees into the community. It is aligned with the Football Association’s Equality policy. The Association is committed to supporting social inclusion through football by bringing people together to overcome discrimination. The national sports sanctions entities have asked all member organisations to develop policies for integrating refugees into their sport. As the governing body for English football the Association recognises the value of sport and the role of football in supporting the development of an inclusive environment for participation to the greater benefit of society. The United Kingdom has committed to taking 20,000 refugees in 2016, with England taking the most. Coming to a new country is not easy when you do not know anyone or speak the language. Refugees may further be affected by trauma. The Association’s integration strategies aim to help in the best way we can and support the ambitions of government and national sporting bodies. This policy and its supporting strategy and guidance will set out a vision for integrating refugees across all levels of our organisation from recreational to the highest professional level. Scope This policy applies to Football Association and all local associations, organisations and clubs affiliated to it. Policy Statement The Football Association is committed to promoting the integration of refugees into UK society through inclusion in its football development programmes and in accordance with the Equality Policy. The Association will engage with member associations, clubs and other stakeholders to develop strategies and allocate responsibilities and resources to achieve this. The Association will monitor performance of the programme and review the effectiveness of the strategy. The policy is fully supported, and will be implemented by the Association’s Main Board. Objectives: · To provide opportunities for refugees of all ages through football which will enhance their quality of life and enable them to achieve to their highest potential. · To promote integration through developing the language skills of refugees and cross-cultural appreciation in a neutral environment though the shared common interest of football. · To work collaboratively with other sports bodies to ensure strategic alignment and complementary programmes. · To identify new opportunities for funding at local, national and international level to support and develop the programme of activities. · To use existing relationships and build new ones with schools, youth centres and retirement homes to benefit the full age range of refugees. · To offer a wide range of opportunities within football to all refugees for all levels of ability and interest. · To encourage and support all parties involved and promote success. Implementation · The FA’s Inclusion Advisory Board, reporting to the Main Board, will oversee the development, implementation, monitoring and review of the refugee inclusion strategy. · The Association will allocate funding for refugee inclusion as part of the overall inclusion budget which will be administered by the Inclusion Advisory Board. · Refugee inclusion will be included in the annual report and action plan on inclusion and anti-discrimination. · A National Refugee Inclusion Co-ordinator will be appointed who will report to the Director of Inclusion. This role will engage with stakeholders, regional associations, national sports bodies and funding agencies to develop, resource, promote and monitor the strategy. · Regional coordinators will be appointed to work closely with local associations and clubs and local government. The roles will identify local needs and opportunities and support applications for resources to provide suitable programmes. · The Regional Coordinators will organise and promote local events and activities and arrange events cascaded down in support of the Association’s national initiatives and programmes. · A budget will be allocated to each region per the number and distribution of refugees. This will be managed by the Regional Coordinators and monitored by the National Refugee Inclusion Coordinator. · Staff and coaches will be appointed to work under the Regional Coordinator on geographic basis per the number and distribution of refugees. Training programmes will be developed and provided to support existing coaches and staff in this aspect. · The staff and coaches will offer support and guidance to the refugees where required. Strategic Plan The Association’s policy for integration of refugees sets out a single vision to enable all refugees to integrate fully into society by 2022. It aspires to make all refugees feel welcome as well as raising health, education and community outcomes. Our strategy sets out our ambition and how we will achieve it, the actions needed to be successful, the role that the Association will play and how we will work with different parties to achieve our shared vision of integrating refugees into our multicultural society. How we will act to deliver the strategic plan: The Association envisages that the whole process for integration could take between 3-5 years and it will be built on these important principles; · Working together: The FA will work with all stakeholders on a national and local level to achieve the utmost success of the integration of refugees into the society. · Being inclusive: The FA will recognise all the cultural preferences of each refugee, considering the range of diversity. · Maximising resources: The FA will ensure that maximum impact is derived from all allocated resources and that everyone involved in the process will get the best value from them. · Reviewing progress: The FA will review progress of the strategy against the annual action plan to monitor that all targets are being met. Football In The Community The Football in the Community programme will be at the forefront of refugee integration. Football in the Community (FITC) is operated under the auspices of the EFL Trust and is therefore Football League related. It is run individually by each of the clubs within the Football League and below. This programme will be used for the initiative since the FITC scheme is well established and respected. It works effectively with local communities and helps improve the lives of many in need through coaching and socialising with others. The FITC scheme would give refugees the opportunity to be associated to the local professional football team and would enable them to play football with people from different backgrounds or to coach others if they would like to. This would then help form a pathway to integrate refugees into the game and the community. To support FITC and to make all refugees feel welcome we would introduce liaison officers and hold regular language sessions to make the transition of integration smoother. The liaison officer would be each refugee’s first port of call should an issue arise or they need someone to talk to. Whilst we envisage that FITC will have a positive impact on integrating refugees, the Association also acknowledges that some refugees arriving will be high calibre athletes. Consequently, the Association would support refugees seeking a professional career in applying for work permits and enable them to look forward to a more stable future. Inclusion through qualification This is a new initiative to be introduced by the FA which offers coaching and refereeing training courses to refugees of all genders and all ages with the primary focus being on social inclusion for refugees living in the region. The course will be free of charge and will be split into theoretical and practical lessons and like the FITC scheme include lessons in English. The ‘inclusion through qualification’ course will act as a fast track into the football world. Refugees will be assisted by language teachers and qualified referees with the assistance of a course guide that includes rich visual media. Refugee Action Board A refugee action board will also be established to help promote engagement and listen to ideas and concerns of all ages. How we will fund the strategic plan: The Association has lead responsibility for delivering and resourcing this initiative. Some initiatives set out in the policy are already underway and have funding allocated. However, funding for new initiatives introduced will come from a redirection of current funding for the game or from identifying new sources. The funding of the strategy will be phased. Each project will receive an initial allocation with further funding subject to performance targets being achieved. · The FITC scheme will be given an initial 1 million GBP in January 2017. Whilst FITC is currently active and funded the scheme will require additional resources to enable expansion into different areas to cope with the influx of refugees. · ‘Inclusion through qualification’ will be allocated 2.5 million GBP at the launch in January 2017. This larger amount reflects that this scheme is new and the cost structure is different. This will cover the appointment of language teachers, liaison officers, coaches and allow support from qualified referees. The initiative will be subject to annual review and the following performance indicators: · Increase in volunteers in the schemes mentioned. · Increase in qualified coaches and referees from ethnic backgrounds. · Increase in participation in football amongst ethnic backgrounds. This initiative will form the basis of the ‘Refugees: World at your Feet’ campaign which sets out a positive vision for integrating the new influx of refugees into society through football . The Association will officially launch this initiative at a presentation evening for all stakeholders. The following table summarises the implementation programme.   I have selected Under Armour as the sports brand to evaluate using the identity prism due to the affinity that I have with them at many levels. Firstly, I admire how the company as risen to prominence, developing over the years in to a major brand through a gradual strategy. In 1999 the brand featured in two American Football films, courtesy of Warner Brothers, with Under Armour launching their first TV add in 2003 (Under Armour, 2016). The advertisement featured three words “protect this house” which acted as a rallying cry to athletes (Under Armour, 2015). Furthermore, it was used for home teams to defend their turf from the opposition in the same way Under Armour protects from competitors. As a result, it attracted a lot more men as well as women to the brand. This kick-started something special as the brand then began acquiring major partnerships such as the Baltimore marathon and partners in Major League Baseball. This is illustrated through the sponsorship agreements that they have had with athletes of increasing prominence over the last decade. In 2006 they were associated with Bobby Zamora (an English footballer who was not that well known outside the UK), whereas Under Armour now has agreements with the likes of Tom Brady (NFL), Stephen Curry (NBA), Michael Phelps (swimmer) and Lindsey Vonn (Alpine ski racer), all of whom are well-established athletes in the US. These types of agreements have helped Under Armour overtake Adidas in the American market (Shah, 2016). The brand in its slogans and adverts mirror my determination to succeed as a person. For example, of their many powerful slogans one is “Our job is to make you better” (R204DESIGN,2013), which acts as a call to arms and suggests to the consumer the notion of Under Armour being on the consumer’s side. It also links to a product performance characteristic, it suggests that the product provides high comfort and better performance when exercising. I also have affinity with Under Armour as I admire their aspiration to be the market leaders in innovation as suggested with “the latest innovation isn’t available yet, but it’s being built at Under Armour” taken from a TV advertisement (R204DESIGN, 2013). Kevin Plank the CEO of Under Armour states that they are not worried about the current competition, “they’re worried about the competition that doesn’t exist yet” (National Retail Federation, 2016). These various statements from Under Armour outline what a forward-thinking organisation they are and how rapidly they are expanding. This is further outlined through their mission statement in which Under Armour expresses its main aim to create “game-changing products to give athletes an advantage” (Under Armour, 2016). When they first launched onto the sports market they solely focused on sporting under garments before expanding into other fields after creating a foothold in that specific field. Below is Kapferer’s brand identity prism and SWOT analysis focussing on Under Armour and how they have become a major sporting brand. Physique is of key importance as this is what the consumer associates with the brand first and foremost. Under Armour’s main physical appearances are the symbol and the logo, otherwise known as the brand mark. According to Brassington and Pettit (2006, p.305) the brand mark is the element (without words) which offers visual brand identity and makes it instantly recognisable. The colour which Under Armour uses for its brand mark according to the colour emotion guide is one to show balance within the brand as well as remaining neutral (Ciotti, 2016). This is shown with product ranges appealing to both sexes and not just being male or female driven. Furthermore, the physique of Under Armour shows a brand which is strong and athletic and being a both indoor and outdoor brand, thus reflecting the neutrality again. The personality of Under Armour is one that is athletic, strong, serious and fit as demonstrated with the sponsorships and the brand ambassadors the company has. They have endorsement contracts with the likes of Andy Murray and Stephen Curry as well as Lindsey Vonn, thus proving that the Under Armour brand does not belong to one specific sex and targets both men and women. The personality can also reflect Under Armour’s will to be the best sports brand as the athletes they have signed up all demonstrate a will to be the best in their specific field. Strong brands are built on strong culture which is what Under Armour portrays with Kapferer (2008, p.183) stating that “every brand should have its own culture to which every product derives”. The values that it relays to the audience are clear and concise, so the consumer knows exactly what Under Armour stands for and more importantly what the Under Armour brand is. Under Armour is firstly an American brand having launched in 1996 with its headquarters in Baltimore. The brand – also projects a modern culture due to its innovative products it producers along with a strong teamwork culture as seen in the brand’s advertisements (i.e. protect this house). The brand portrays its relationship to its consumers through a number of eye catching slogans which gets the audience hooked. On the brand identity prism, there are such slogans as “I will” which immediately fills the consumer with empowerment and a drive to succeed. The phrase also portrays that the brand is for winners and wants to strike a winning mentality amongst its consumers. Reflection is the view of the sender and how it is representative of them. The brand identity prism shows that Under Armour wishes to demonstrate that with the right application anyone can succeed through the underdog tagline. This would have a wide appeal as people do generally have an affinity with the underdog and the prospect of success against the odds along with being highly competitive. Under Armour also reflects an image which is successful and fitter suggesting that if you wear our brand you too can be seen as a more fit and successful person. This reflection shows that Under Armour wishes to work with the consumer through having a broad appeal and that if the consumer puts in the hard work it will pay off, thus becoming fitter. The self-image which Under Armour wishes to show is one of innovation with high quality within their products. This gives the impression to the consumer that when they purchase an Under Armour product it will be of leading quality in design and performance. The innovation part is important as they try to distinguish themselves from other sports brands by leading in innovation - most consumers love to try something new on the market. Furthermore, the brand wants to show everything that the company produces is of high calibre meaning that the price of the products is worth it as it aims to satisfy the consumer by giving them the ultimate comfort and enjoyment from it. References

Brassington, F. and Pettit, S (2006). Principles of Marketing. London: Pearson Education Limited. p305. Ciotti, G. (2016). The Psychology of Color in Marketing and Branding. Available: https://www.entrepreneur.com/article/233843. Last accessed 6th Dec 2016. Farhana, M. (2014 ). Implication of Brand Identity Facets on Marketing Communication of Lifestyle Magazine: Case Study of A Swedish Brand. Journal of Applied Economics and Business Research. 4 (1), p23-41. Gaines, C. (2016). Under Armour has a brilliantly simple strategy to do something Nike has been unable to do — conquer the golf world. Available: http://www.businessinsider.com/how-under-armour-plans-to-do-something-nike-failed-to-do-conquer-the-golf-world-2016-3?international=true&r=US&IR=T . Last accessed 7th Dec 2016. Kapferer, J.N (2008). The New Strategic Brand Management. 4th ed. London: Kogan Page Limited . p158-189. Kapferer, J.N (2012). The New Strategic Brand Management. 5th ed. London: Kogan Page Limited. p182-193 National Retail Federation. (2016). How Under Armour Is Changing The Way Athletes Live. [Online Video]. 5 February 2016. Available from: https://www.youtube.com/watch?v=IOkzta6p8ME. [Accessed: 30 November 2016]. R204DESIGN . (2013). Under Armour retail concept . [Online Video]. 19 February 2013. Available from: https://www.youtube.com/watch?v=vdTPqPzvK9g. [Accessed: 30 November 2016]. Shah, O (2016). ‘Are Nike and Adidas under pressure from Under Armour?’, The Times Style. 28 August 2016. p20-21. Smith, G. (2015). Putting an End to a Preventable Scourge. Available: https://www.whitehouse.gov/blog/2015/02/26/putting-end-preventable-scourge. Last accessed 5th Dec 2016. Under Armour. (2015). Our history. Available: http://www.underarmour.jobs/why-choose-us/our-history/. Last accessed 4th Dec 2016. Under Armour. (2016). The UA story: story. Available: http://www.uabiz.com/company/history.cfm. Last accessed 4th Dec 2016. On deciding who to focus on for the personal brand an interesting observation was that athletes who are successful brands position themselves differently depending on the sport they are associated with. For example, a rugby player may position themselves as being sophisticated, sharply dressed and gentlemanlike whereas a basketball player may want to brand themselves as being very hip and street (fashionably current and cool) in order to appeal to that sports-specific audience. Furthermore, even athletes within the same sport position themselves differently which is how they variously attract endorsements from rival brands such as sport clothing companies like Nike, Adidas or Under Armour.

Stephen Curry, in my view has developed into a very reputable and valuable brand over recent years, building up a successful brand portfolio thanks partly due to success on the court. His achievements over a recent period have helped to establish him as one of the best players in the league, thus attracting attention from global brands. The reason why I think he has become a reputable brand is because he has managed to distinguish himself from other big name Basketball player brands such as Lebron James and Kobe Bryant. Unlike James and Bryant who are both seen as very “in trend” in terms of fashion and slightly edgy, Curry’s appeal is in demonstrating a positive lifestyle that is at the heart of a number of charity campaigns

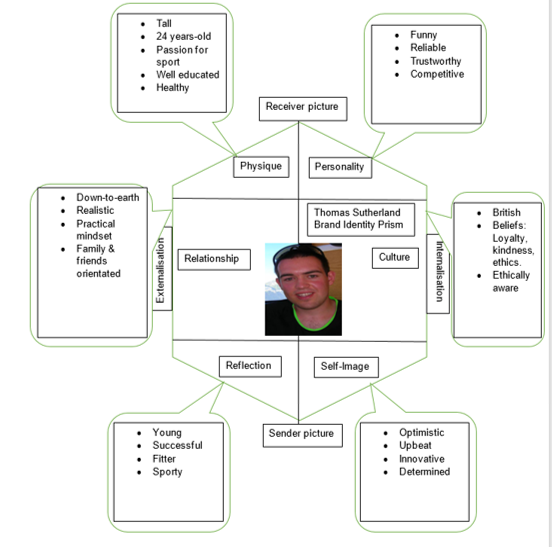

Brands may be distinguished through their different components. Similarly analysing each person as a brand will reveal different characteristics. Physically someone may be male, while another is female, one may have blue eyes the next green eyes. Also the way we portray ourselves varies as some are very outgoing, others are shy, and some people have a very sporting personality with fitness and keeping in shape being important for them. The point is that everyone is unique with potential to stand out. The brand identity prism shows this through six elements which we can analyse a brand such as a major retailer or in this case ourselves, an athlete and a sports team or a sports company.

“Brand personality has been the main focus of brand advertising since 1970” (Kapferer, 2008, p.159). The personality of the brand concerns how the brand portrays itself through its characteristics. Various methods can demonstrate these, for example the colour scheme used, the logo or the style of writing. Also, the brand could portray itself through brand endorsement in an advert. This allows the consumer to identify with the endorsing person that reflects the brand and then compare and align it to themselves. Personality is arguably one of the most important elements of the prism as it gives a brand a human identity, characteristics if you would. The way I try to portray myself is a very kind and humorous person which can also help to show a warmth and welcoming presence. Another part to my personality is being reliable, gentle and trustworthy which again shows a warm presence and demonstrates that the brand can be trusted by the consumer and hopefully endears itself to them. I am also competitive meaning that I strive for the best and persevere, which would appeal to the customer knowing that they are getting a quality brand that wants to compete with the other brands in the same field. The culture of the brand is in essence the values and principles that underpin it. For example, certain brands reflect the country of origin as with the reputation of German cars. Kapferer (2012, p.160) states that the “cultural facet of brands’ identity underlines that brands are engaged in an ideological competition”. Using the culture element of the identity prism on myself, a key part of this is being British as until now I have spent my whole life living there. This infers an association with British values and culture and their perception, where if the British brand is damaged this could cause negativity for my brand. However, culture can be seen as much more than just national identity, it can represent beliefs of the brand and what its ideology is and aspirations for the consumer. My main beliefs as a brand would be loyalty, kindness, social conscience and ethics, which would be reflected in the consumer of the brand. These four beliefs interlink as together they reflect a strong brand that aims to get the consumer’s trust and confidence so that over time they develop the same loyalty that the brand represents. Acting in an ethical way is a key element. The relationship part of the prism would position me as very down-to-earth, which means that I am very realistic person and have a practical mindset. Part of this is being family and friends orientated, underling that I am a very caring person so as a brand I would care what the consumer thinks. Also by having these close links (i.e. with family and friends) illustrates the brand would have close ties with its customers and thereby gain the consumer’s brand loyalty and the relationship would reward that loyalty and mirror it. This reinforces the culture dimension of the brand. Reflection is part of the constructed receiver part of the prism (how others see me) and develops an image over time that reflects the buyer. It is what image the buyer would like to be associated with and aspires to as opposed to what they are known for. The brand that would be reflective of me and thus the buyer would be one that represents being fitter, younger, ethical and successful. This would not necessarily appeal to every young successful person who is active, but it would appeal to people aspire to be like that and be associated with this particular brand. For example, the brand does not target the older generation, however they may buy it because of the association of being younger, successful and active and may feel these characteristics as a result of buying the brand. Self-image, just like reflection, is in the receiver part of the prism and is related to how the consumer feels about the product and their association with it. Many brands make the consumer feel differently, for example people who buy the drinks brand Pepsi feel cool and smart, whilst people who purchase a BMW feel powerful and important. In my view the brand which I represent would make the consumer feel optimistic and upbeat and that they are trying something innovative (leaders in innovation). It would make the consumer believe that they are in charge of their own destiny and able to make bold decisions without being judged. Although the consumer would not feel wealthy and up market it would however give them a sense of comfort and belonging to a respectable brand.

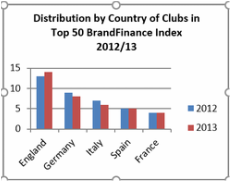

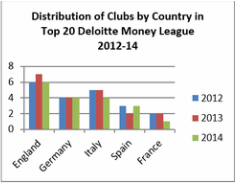

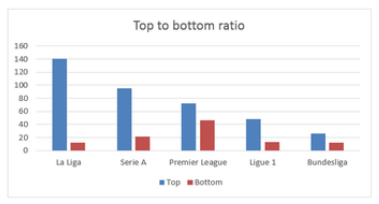

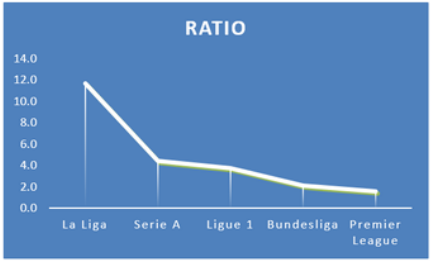

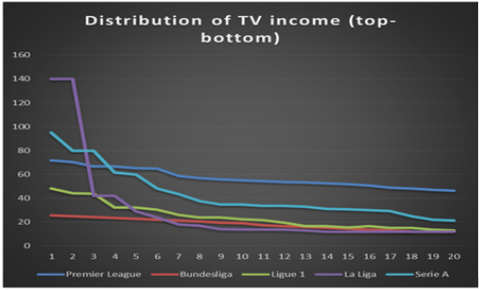

This dissertation would not have been possible without the support of the University of Hull and most importantly my dissertation supervisor Richard Andrews. Firstly the University of Hull have gave me support over the 4 years which has allowed me to progress, develop my skills and ultimately finish my degree in business management. Also I would like to further than the University for allowing me to do a topic for my dissertation which I feel really passionate about and hold a major interest in. Secondly I would to thank Richard Andrews, my dissertation supervisor, whose support and encouragement has enabled me to produce this report through his academic guidance. Furthermore the various discussions held with Richard Andrews helped narrow the ideas and thoughts down and transfer them into the final report. Abstract Financial regulation has been present in a number of European leagues for some time now and other leagues are following suit as UEFA introduce their Financial Fair Play to introduce fairness between clubs while at the same time keeping the competiveness with each club. The increased interest of football globally means every club has an opportunity to generate further revenue as they look to gain a share in the global football market. However in order to increase revenue, each club needs a respectable strong brand which will attract more fans to invest in their product. But as clubs try to develop a strong brand, they take investment risks which do not always pay off and leaves the club with severe debt on occasions. With these inevitable risks it is more important than ever to introduce financial regulation that will safeguard each clubs future. It is further important to have these regulations as clubs in some cases spend vast amounts of money in trying to achieve success as they know the reward is huge. The report provides analyses of how financial framework and brand value interlink with each other and how by implementing or not implementing financial regulation effects the league as a brand. The study comprises all of the ‘Big 5’ leagues in Europe (England, France, Germany, Italy and Spain) and compares the amount of or lack of regulation in each of the five countries in terms of income streams and total revenue, while also taking into account average attendances in each of the leagues and varying ticket prices. The literature review comprises of various sources such as recent articles, books and journals which help build up the overall picture and contribute towards a balance view which ultimately contributes to the conclusion of this thesis. The various authors cited within this text have vast amounts of experience and are widely respected within this this area which helps with the validity of the research. The methodology uses a secondary approach as this was deemed the appropriate method to use which allows the most accurate results and reasonable outcomes to be reached. Within the methodology the various approaches rely upon brand finances ‘brand value’ index which takes into account various factors in order to interpret the overall outcome that is the value of the brand. The findings take into account the results from the method along with the information gathered from the various resources used. They outline that financial regulation is a vital tool within the World of football nowadays and highlights the differing financial results within the 5 countries. 1. Introduction The aim of this thesis is: ‘To investigate the impact of the model of financial regulation in football on the successful development of the league as a brand’. This outlines the bigger problem in the football industry as brand has become of increasing, if not dominant, significance in developing its commercial exploitation reflecting its globalisation. Football is generating ever increasing revenue, especially at the top end, yet many leagues and clubs are running at increasing losses. There is also disparity in revenues within the leagues and many teams overspend to try to achieve success, although ultimately many fall short and end up in debt. However as Thompson (2013) stated it shouldn’t matter if clubs have debt as they can be seen as different from other businesses. Furthermore a number of clubs in some leagues have been bought and heavily subsidised by wealthy private investors. The football authorities at national and transnational levels are increasingly concerned about the sustainability of clubs and competitions running at high levels of debt and are introducing financial regulations to limit these losses. This thesis investigates whether financial regulation can go hand in hand with the brand through examining the following four key objectives: • Examination of the impact that the relatively well established financial regulations in the French league have had on its development as a brand. • Comparison of the French League with other variously regulated major European leagues, such as the other four “big 5” (Desbordes, 2006. P.83) (England, Germany, Italy and Spain). • Investigation of relative brand value by comparing the revenue streams of indicative clubs in the French League with those of similar level teams across Europe. • Assessment of the potential effect of UEFA Financial Fair Play Regulations on a League’s brand. From this it should possible to conclude whether financial regulations can be a positive or negative influence for the football industry and for the brand of the leagues and their clubs. Over the last 10 years finance in football has become increasingly important with some clubs spending beyond their means, subsequently going out of business. Finance in football is important to each club as this helps dictate the strength of the brand, with research into brand equity being conducted since the 1980’s, due to the competiveness and link to market value (Bridgewater, 2010). Trends in brand value and presence in the Deloitte top 20 over recent years are shown in charts 1.1 and 1.2. Further information is contained in appendices 1.A & 1.B.

With this has come a need to monitor finance in football as according Hamil and Walters (2010) European football significantly lacks profitability and financial management, with King (2011) stating that financial troubles have followed as a despite income rising in the ‘Top 5’ leagues. Many argue that financial regulation is unnecessary and clubs should be allowed to control their own affairs, with owners, fans and shareholders backing their club regardless of the financial state it is in. However recent work by Beech (2008) states that despite an increase in revenues many clubs still operate in the red and that the situation in England mirrors that of European football in general with Italy being one of the countries with the worst financial management, the other, according to Gomez et al (2011), being Spain. Andreef (2007) reports that despite rising debt levels within the Spanish game, clubs increase spending on transfer fees and player wages. This view is echoed by Kuper and Szymanski (2012) who state that many supporters have been worried about their clubs financial state for over a decade, with people becoming increasingly worried after the recession. An example pointed out by Kuper and Szymanski is that Chelsea and Manchester United’s combined net debt levels when they met in the 2008 UEFA Champions League final stood at £1.3 billion. This was a worrying sign, so worrying that in 2009 UEFA President Michel Platini stated that if this trend continued it would not be long before major European clubs faced going out of business. These concerns have been taken seriously as in 2012 UEFA announced their intention to introduce Financial Fair Play (FFP) which would mean clubs would have to be more stringent with their finances. However, contrary to Platini’s concerns, Kuper and Szymanski (2012) state that the idea of football clubs being “inherently unstable” (Kuper & Szymanski, 2012. P.81) is wrong as they rarely go bust despite being “incompetently run” (Kuper & Szymanski, 2012. P.81). Furthermore Kuper and Szymanski (2012) state that the various football authorities worry too much about finances of clubs and are often concerned about the wrong clubs. This sentiment is supported by a comparison between the 1923 English Football League and the 2007-2008 season, where 97% of clubs (85 clubs) that competed in 1923 still competed today. Furthermore 75 of the clubs still remained in the Football League (top 4 divisions) and quite astonishingly 48 of the clubs were in the exact same division as 1923 (please note this may of changed from 2008). Also only 9 clubs from 1923 had moved divisions by 2 or more. These figures support Kuper’s and Szymanski’s argument that football clubs are unstable but rarely go bust, which begs the question should financial regulation be for all clubs in the beautiful game or not? Furthermore if European clubs’ debt did cause them to collapse then “surely there would now be virtually no European football clubs left” (Kuper & Szymanski, 2012. P.89). However Beech, Horsman and Magraw (2007) argue that recent research has shown worrying incidence of English clubs facing insolvency. Between the years of 1986-2007 there have been 56 clubs becoming insolvent (68 in total as it happened more than once with some) (Beech et al, 2007). In part the figures were influenced by ITV Digital’s (then TV rights broadcaster) collapse in 2002 which had a disastrous effect on the Football League clubs, however Hamil and Chadwick (2010) state that more significant factors affecting solvency were poor on field performance and relegation. The main problem Hamil and Chadwick (2010) identify is that English football has failed to deal with the commercialisation of the sport, since only in the last 10 years have clubs “come to terms with a post-commercialised phase” (Hamil & Chadwick, 2010. P.260). However whilst the Premier League has adapted to the business needs of the industry, this has been not entirely successful. Despite the considerable revenue streams which have been created and spent by clubs, the control of costs to guarantee profit has proved very difficult. Financial sustainability has consequently appeared on the agenda of regulatory bodies. Most notably UEFA has introduced Financial Fair Play (FFP) criteria for the 2013-14 season, which restricts clubs to a €45M cumulative loss over 3 years and a maximum loss (if the owner does not inject equity) of €5M over the same period (Thompson, 2013). Participation in UEFA’s club competitions (Champions League & Europa League) (UEFA, 2014) is dependent on meeting these requirements with UEFA monitoring each clubs accounts for compliance. Furthermore, according to Conway (2014,) clubs cannot spend more than their generated revenue and they are expected to meet all their transfer and employee payment needs. The sanctions in place for any club breaching the rules range from warnings and fines to a ban from UEFA competitions. An investigation of 76 clubs competing in this season’s (2013/14) Champions League and Europa League thought to be breaching the regulations has been completed although the evidence will not be released until the end of the season with the first action being taken in April 2014. Michael Desbordes has researched financial regulations in the French league over recent years. Desbordes (2006) states that the French method of managing finance is unique and aims to avoid bankruptcies part way through the season, which makes the league a “true championship” (Desbordes, 2006. P.86). Similar systems to the one in French football are used in rugby, handball and basketball. The Direction Nationale du Contrôle de Gestion (DNCG) is the system which monitors French football finance and is an internal commission to the French Football Federation (FFF). Desbordes (2006) cites that the system acts like “French football’s policeman” (Desbordes, 2006. P.86). The tight financial regulations tie into increased value of TV deals with Desbordes (2010) stating that Ligue 1’s TV deals have increased from the end of the 1990’s through “two successful deals” (Hamil & Chadwick, 2010. P.303). According to Repition (2008) the deal signed in 2008 enabled clubs to share €668 million. Furthermore the latest deal signed in April 2014 for the 2016-2020 seasons saw the sum increase again with the rights for Ligue 1 going for €726 million and the Ligue 2 (2nd tier) for €22 million each year (LFP, 2014). Comparison with the Spanish League (La Liga) shows a contrasting situation with looser financial regulations and many clubs in the top flight holding severe debt. However according to Ascari and Gagnepain (2006) Spanish football has seen significant economic activity with its matches being well attended. This is supported by statistics which shows La Liga had the 4th highest average attendances for the 2007/08 season in Europe (Deloitte, 2009. P. 14), and the 3rd largest revenues overall from TV broadcasting (Deloitte, 2009. P. 13). However there is a lack of competitiveness since up to the 2007/08 season, 77 league championships had taken place, but only 9 teams in that time won it. Indeed 3 of the 9 have only won it once (Sevilla FC, Deportivo de la Coruna & Betis) with the majority of league championships going to either Barcelona or Real Madrid (Hamil & Chadwick, 2010). Marti et al (2010) state that the increasing wealth generated by a few football clubs in Spain could lead to an increasing imbalance in the league. Marti et al (2010) suggest further that participation in International competition goes someway to explaining the financial imbalance with only a few clubs obtaining a large amount of money. Gomez et al (2008) supports this view by acknowledging that the “existence of an elite International competition (e.g. UEFA Champions League), automatically creates imbalance in the national competitions” (e.g. La Liga) (Hamil & Chadwick, 2010. P.267). Italy is another of the ‘big 5’ leagues with financial difficulties. This is evident in the recent Deloitte Money League (2014) which states that Italian clubs, apart from Juventus, are struggling to grow resulting in them sliding down the Money League. Deloitte (2014) highlights the fact that with the majority of clubs not owning their stadiums this makes it difficult for them to generate match day and commercial revenue on par with other clubs in the ‘big 5’. Furthermore Cherubi and Santini (2010) echo this view by stating that the economic financial situation is dire in every area apart from broadcasting income upon which clubs are “highly dependent” (Hamil & Chadwick, 2010. P.291). However it is worth noting that like Spain the country’s poor economic climate has had an impact. Germany on the other hand has tighter regulations like France with many clubs being debt free. This is partly down to the various governing bodies which regulate different levels of German football. These governing bodies include the German Football Association (DFB) which regulates the game generally, then within that is the Fussball Liga GmbH (DFL) which governs the Bundesliga (1st & 2nd tier). According to DFL (2008) the annual turnover of the Bundesliga in 2007 was €1.45 billion, with Buhler (2010) stating that the Bundesliga is “considered one of the most business-like leagues in the World” (Hamil & Chadwick, 2010. P. 327). Buhler (2010) states that German football saw major growth throughout the 1980’s with the introduction of privately owned TV companies, which led to more competition in the broadcasting market resulting in higher income streams for the clubs. A further rise in revenue from broadcasting rights was seen in the 1990’s with the introduction of pay-per-view. Other success factors in Germany include high attendances and cheap ticket prices which in turn help generate healthy revenue. Financial regulations are also being introduced in England with FFP applied to the English Premier League and Championship (1st & 2nd tier) for the 2013/14 season. This supplements existing regulations for England’s League 1 and League 2 (3rd & 4th tier). The Premier League FFP include a maximum of permitted losses of £105M over 3 seasons, while the maximum loss is £15M should the owner not inject equity (Thompson, 2013). There are no restrictions on wages if they are below £52M per annum. Each club will be monitored through their annual accounts along with the clubs’ projections which will be submitted to the Premier League at the end of each season. An aspect of financial regulation is the effect on the brand. Bridgewater (2010) looked into the development of football as a brand. The importance of brands to business and to marketers has increased over recent decades with developments in branding in a broader range of sectors (public sector, charities & e-markets), which ultimately gives the customer something that they can identify with. Brand value in football has an essentially emotional basis. Bridgewater (2010) examined the evolution of the support base from local allegiances in early times into modern global tribes, i.e. groups with shared interests. Part of the value to the supporter was suggested as lying in the escapism and the sense of belonging to a community that it offers. Furthermore Cova (1997) identified the role of the shared interest amongst the supporters and the effect on their self-esteem and suggested that brand value lies in a product’s “linking value”, that is its ability to bind this wider community. One example of this is Manchester United whose global marketing strategy has made it as familiar globally as Coca-Cola. Bridgewater (2010) states that the “sporting world has long recognized the fervent loyalty of fans” (Bridgewater, 2010. P.2) concerning a certain team or a sporting icon. This view is illustrated by League Two (4th tier) Luton Town taking 40,000 fans to Wembley for their Johnstone’s Paint Trophy Final. However commercial significance also plays a key part in brand growth. The view of brand being vitally important in the sports industry (particularly football) nowadays is outlined by Ozanian (2005) who stated that the global sports market is worth around $12 billion per year, whereas Bridgewater (2010) stated that the sports market in the United Kingdom in 2008 was estimated to be worth £21.2 billion and growing year upon year. Furthermore Haigh (2013) states the average amount of money paid by sponsors to be associated with 1 of the top 50 clubs increased in 2013. The analyses for this thesis will be based on secondary data relating to the two complementary strands of finance and brand value. By drawing on published data this approach should ensure more accurate, and in some cases tested, information on which to make comparisons. Furthermore the use of secondary data is less time consuming compared with that of primary as there is no use of interviews, which also means there is no reliance on an extra party which may have a detrimental effect on the research, for example through bias or context. Although the thesis uses secondary data only, the researcher has not neglected the HUBS ethical procedures and abided by all the rules (see appendices A for ethics proforma.) In assessing the ‘Big 5’ leagues the factors to be considered are the regulatory framework including the negotiation mechanisms for broadcasting rights; financial indicators such as the value, sources and distribution of revenue, and profitability; and indicators of brand value of the leagues and the clubs such as attendances, commercial and broadcast revenue and sporting competiveness of the leagues. The information is taken from published sources such as core texts and articles relating to football finance and the annual reports of the governing bodies such as UEFA, which should be considered to be reliable and authoritative. Another resource is the index analyses by BrandFinance which assesses the strength of clubs as a brand. The index analysis helps to “benchmark strengths, risks and future potential compared to their competitors” (Haigh, 2013. P.27). Clubs are rated from AAA+ to D for brand strength (strong to weak). Key Performance Indicators (KPI’s) are also used in this to distinguish whether or not a club has a strong brand. These KPI’s consider 5 factors, namely the star players at the club which drive sales of the merchandise; the stadia in which the club’s “product is showcased” (Haigh, 2013. P.27); the club’s heritage which determines how loyal the fans are; trophies won, as Haigh (2013) states that “only history remembers winners” (Haigh, 2013. P.27); and the manager of the team as the club cannot have a strong brand with an un-successful manager or if there is managerial instability within the club. Deloitte’s Money League provides a method for comparing a club’s financial strength. Deloitte releases the Money League annually enabling comparison against previous years to test a clubs success both on and off the field. There are various ways in which relative wealth of clubs can be determined although these can be limited by information not being in the public domain. Deloitte (2014) has developed models which help to predict clubs future cash flow which assists sellers and potential investors. The easiest way according to Deloitte (2014) to test a clubs wealth is through revenue which is the easiest comparable information as well as it being widely available. The following sections outline the various regulatory bodies in each of the ‘Big 5’ countries, indicators of financial health and measures of brand value from various teams across the ‘Big 5’. Ticket prices and attendance figures are also considered. Appendix 4.A shows the Deloitte (2014) Money League analysis of top 20 teams accompanied by a table it showing the country that the majority shareholder is from. The value of TV revenue within each league and its distribution is included as a measure of financial performance and is shown in figures 4.1, 4.2 and 4.3 below, which enables comparison across the leagues.  Figure 4.1 TV revenue distribution €M (top-bottom).  Figure 4.2 TV revenue distribution ratio (top-bottom)  Figure 4.3 Distribution of TV income €M (top-bottom) 4.2.1. Regulatory Framework In France the clubs’ finances are monitored by the DNCG. This organisation requires the member clubs (top 5 divisions) in the league pyramid to submit their accounts at the end of the season. If a club fails to abide by the rules the sanctions that the DNCG can impose include point deductions and demotion of leagues and in some cases expulsion. France’s TV rights are distributed evenly thus mirroring that of England and Germany. The rights are split 50:25:25 with 50% being split in equal parts, 25% based on the television audience and 25% on sport merit which is related to the clubs previous seasons positions. 4.2.2. Financial Performance Many clubs in France still have debt with an increase from 2011-12 season. The average club debt overall was €60M, however 3 of the 20 clubs in Ligue 1 did have positive results. Ligue 1 revenue rose €1.27 Billion (11.4%), but this was predominantly down to PSG and their relationship with Qatar Tourism Authority.

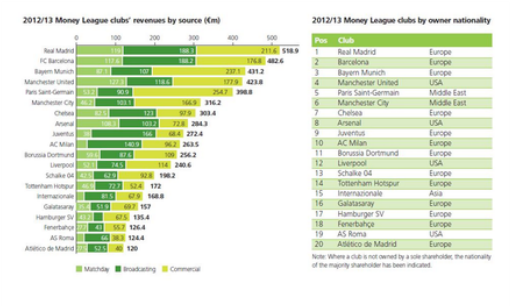

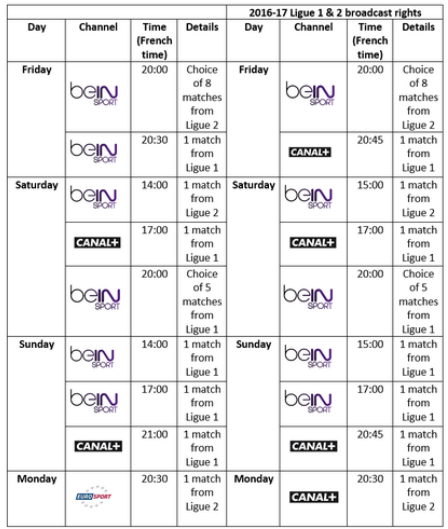

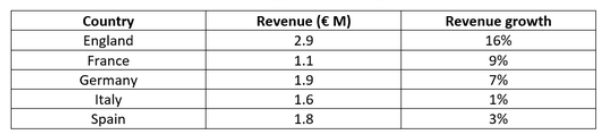

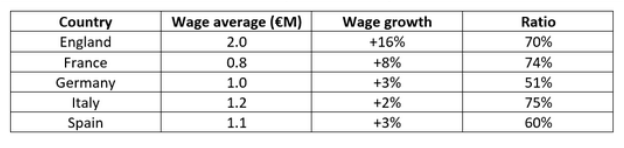

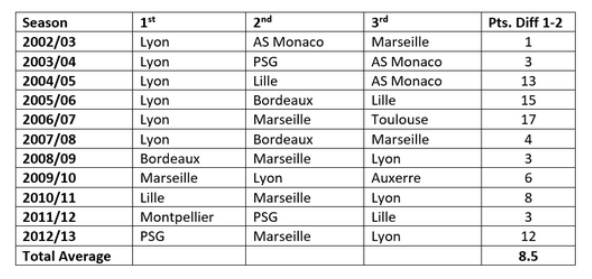

4.2.3. Brand Value The French league has fared the worst out of the “Big 5” as some teams cut back finances due to lack of on the field success. There are only 4 out of 20 Ligue1 clubs in the top 50 and a worrying sign is all the 4 brands have decreased in value. The Deloitte Money League 2014 (Deloitte (2014)) shows only one French team in the top 20 (PSG) with Marseille dropping from 17th position down to 30th, while Lyon have even fallen outside the top 30 due to missing out on a Champions League place. In comparison the previous Deloitte Money League (2013), placed 2 French Clubs in the top 20 (Olympique Marseille and Olympique Lyon), whereas in 2014 only PSG features. Based on the 2013 Money League, Marseille’s revenue dropped by 10% to £109.8M with the club having a mixed season on the pitch. Whereas Lyon for 2011/12 saw revenue drop by 1% to £106.7M due to decreases in both match day and commercial revenue with them having the second lowest matchday revenue in the Deloitte Money League top 20 2011/12. However this decrease was offset by Lyon’s rise in broadcast revenue. Their main failing was finishing 4th in their domestic league meaning failure to qualify for the Champions League for the first time since 1999. The prediction in Deloitte’s Money League (2013) that Lyon would struggle to maintain a top 20 place for the Money League in 2014 has been proven right. PSG’s revenue has grown substantially from £178.4M in 2012 to £341.8M in 2013. Contributing to this was the acquisition of global brand name David Beckham. Paris Saint-Germain is the highest ever French team in 5th place of the Deloitte Money League due to their “record turnover of €400 Million” (Deloitte, 2014. PP. 18) due to the enhancement of their global brand since the Qatar Sports Investment takeover in June 2011. Kay (2014) states that UEFA’s FFP will test them, having only being allowed to make loses of £37 million. However according to Kay (2014) they have signed a deal with Qatar Tourism Authority worth £570 million over 4 years which should cover their accounts for the years 2012 to 2016. The challenge however is whether UEFA deem the sponsorship unfair due to a possible connection with the owners. In comparison another French giant, Marseille, has been towards the bottom of the Deloitte Money League for the previous five years having peaked at 14 and as low as 16. Despite Marseille winning the League Cup and managing to reach the ¼ finals of the Champions League, the club finished a disappointing 10th place meaning that they only qualified for the UEFA Europa League as virtue of winning the cup. Furthermore the renovations at Marseille’s stadium caused the capacity to be reduced temporarily resulting in a drop in match day revenue by 29% to £14.6M. Ticket pricing influences the picture. Spiro (2013) states that inflated prices are not an issue in France as the clubs try to attract as many fans as possible since only a minority of games sell out. Furthermore Spiro (2013) outlines that for the majority of Ligue 1 teams, spectators can get in for less than €20 (£16.70), with a number of teams allowing spectators in for half of that. It is also worth noting that due to their recent success Paris Saint-Germain has seen an increase in season ticket holders from 10,000 to 31,000. This is despite prices rising at the Paris based club with prices rising over the last 2 years by 11% and 30% respectively. A future impact on the French Ligue 1 brand is the importance of broadcasting rights. The new deal starting from 2016 will provide even more money to share between the teams. This sees a 20% rise from the previous contract, with LFP president Frederic Thiriez stating he wants a “league on the podium of the three best European nations” (LFP, 2014) behind Germany and Spain. Thiriez further states that the deal sees the LFP keep their two major broadcasting partners (Canal+ & BeIn Sports) for the next six seasons. Furthermore by having a record sum for the seasons of 2016 to 2020 its makes “Ligue 1 one of the most valuable leagues in the Word” (LFP, 2014), which can only be seen to enhance the brand. More detail on the new deal can be found in Appendices 4.B. 4.3.1. Regulatory Framework Germany has a similar system to France in that it monitors clubs finances through their submission of accounts and transfer documents. Punishments in Germany should a team enter the red involve point deductions and transfer embargos. The system was created by the DFL and acts as a prototype for UEFA’s licensing scheme as well as being seen as a beneficial model to other countries. The criteria monitored by the DFL include five categories (sporting, infrastructure, personnel and administration, legal and financial) (Buhler, 2005). In 2007/08 as a result of these strict regulations all 18 Bundesliga clubs were financially stable and reporting profits (DFL, 2008. P.173), thus highlighting its success. Broadcasting rights are negotiated between the DFL and broadcasters which allows the revenue to be distributed evenly amongst the clubs in the Bundesliga. 4.3.2. Financial Performance Germany had the second biggest revenue growth out of the ‘Big 5’, these results can be seen in appendices 4.E (4.F shows wage average). The Bundesliga’s main growth in revenue was the success of commercial deals which accounted for over half of the clubs revenue.